Page 706 - Krugmans Economics for AP Text Book_Neat

P. 706

However, the two versions of long-run equilibrium are different—in ways that are

economically significant.

Price, Marginal Cost, and Average Total Cost

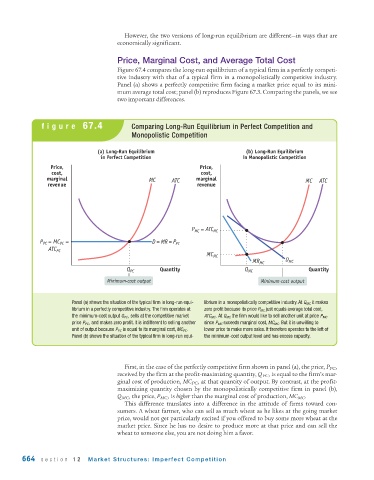

Figure 67.4 compares the long-run equilibrium of a typical firm in a perfectly competi-

tive industry with that of a typical firm in a monopolistically competitive industry.

Panel (a) shows a perfectly competitive firm facing a market price equal to its mini-

mum average total cost; panel (b) reproduces Figure 67.3. Comparing the panels, we see

two important differences.

figure 67.4 Comparing Long-Run Equilibrium in Perfect Competition and

Monopolistic Competition

(a) Long-Run Equilibrium (b) Long-Run Equilibrium

in Perfect Competition in Monopolistic Competition

Price, Price,

cost, cost,

marginal MC ATC marginal MC ATC

revenue revenue

P = ATC MC

MC

P = MC = D = MR = P PC

PC

PC

ATC PC

MC MC

MR MC D MC

Q PC Quantity Q MC Quantity

Minimum-cost output Minimum-cost output

Panel (a) shows the situation of the typical firm in long-run equi- librium in a monopolistically competitive industry. At Q MC it makes

librium in a perfectly competitive industry. The firm operates at zero profit because its price P MC just equals average total cost,

the minimum-cost output Q PC , sells at the competitive market ATC MC . At Q MC the firm would like to sell another unit at price P MC

price P PC , and makes zero profit. It is indifferent to selling another since P MC exceeds marginal cost, MC MC . But it is unwilling to

unit of output because P PC is equal to its marginal cost, MC PC . lower price to make more sales. It therefore operates to the left of

Panel (b) shows the situation of the typical firm in long-run equi- the minimum-cost output level and has excess capacity.

First, in the case of the perfectly competitive firm shown in panel (a), the price, P PC ,

received by the firm at the profit-maximizing quantity, Q PC , is equal to the firm’s mar-

ginal cost of production, MC PC , at that quantity of output. By contrast, at the profit-

maximizing quantity chosen by the monopolistically competitive firm in panel (b),

Q MC , the price, P MC , is higher than the marginal cost of production, MC MC .

This difference translates into a difference in the attitude of firms toward con-

sumers. A wheat farmer, who can sell as much wheat as he likes at the going market

price, would not get particularly excited if you offered to buy some more wheat at the

market price. Since he has no desire to produce more at that price and can sell the

wheat to someone else, you are not doing him a favor.

664 section 12 Market Structures: Imperfect Competition