Page 5 - NorthAmOil Week 29 2021

P. 5

NorthAmOil COMMENTARY NorthAmOil

suggests the only logical buyers would be Can- nonetheless remains one of the more polluting

ada’s Final Four operators,” he said, also noting segments of the global oil industry. At the start

that he expected oil sands assets to be the first to of this year, consultancy Rystad Energy said that

come to market as super-majors seek to reshape the average carbon dioxide (CO2) intensity for

their portfolios. the oil sands was 73 kg per barrel of oil equiv-

Speaking to Canada’s Financial Post, Craig alent, compared with 12 kg per boe for shale

said the CAD13.4bn price tag was a conserva- output.

tive estimate.

“They may be worth much more than what What next?

we put in, but could be sold for much less,” he It would thus not be surprising if oil sands sales

said. are announced over the coming months. Already

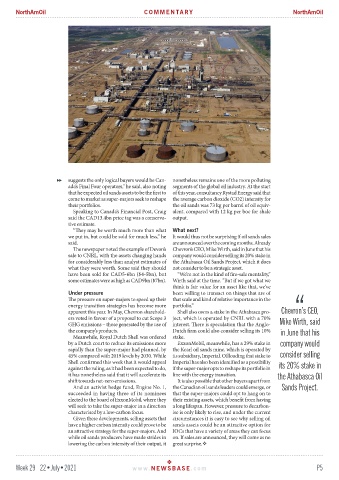

The newspaper noted the example of Devon’s Chevron’s CEO, Mike Wirth, said in June that his

sale to CNRL, with the assets changing hands company would consider selling its 20% stake in

for considerably less than analyst estimates of the Athabasca Oil Sands Project, which it does

what they were worth. Some said they should not consider to be a strategic asset.

have been sold for CAD5-6bn ($4-5bn), but “We’re not in the kind of fire-sale mentality,”

some estimates were as high as CAD9bn ($7bn). Wirth said at the time. “But if we got what we

think is fair value for an asset like that, we’ve

Under pressure been willing to transact on things that are of

The pressure on super-majors to speed up their that scale and kind of relative importance in the

energy transition strategies has become more portfolio.”

apparent this year. In May, Chevron sharehold- Shell also owns a stake in the Athabasca pro- Chevron’s CEO,

ers voted in favour of a proposal to cut Scope 3 ject, which is operated by CNRL with a 70%

GHG emissions – those generated by the use of interest. There is speculation that the Anglo- Mike Wirth, said

the company’s products. Dutch firm could also consider selling its 10% in June that his

Meanwhile, Royal Dutch Shell was ordered stake.

by a Dutch court to reduce its emissions more ExxonMobil, meanwhile, has a 29% stake in company would

rapidly than the super-major had planned, by the Kearl oil sands mine, which is operated by

45% compared with 2019 levels by 2030. While its subsidiary, Imperial. Offloading that stake to consider selling

Shell confirmed this week that it would appeal Imperial has also been identified as a possibility

against the ruling, as it had been expected to do, if the super-major opts to reshape its portfolio in its 20% stake in

it has nonetheless said that it will accelerate its line with the energy transition. the Athabasca Oil

shift towards net-zero emissions. It is also possible that other buyers apart from

And an activist hedge fund, Engine No. 1, the Canadian oil sands leaders could emerge, or Sands Project.

succeeded in having three of its nominees that the super-majors could opt to hang on to

elected to the board of ExxonMobil, where they their existing assets, which benefit from having

will seek to take the super-major in a direction a long lifespan. However, pressure to decarbon-

characterised by a low-carbon focus. ise is only likely to rise, and under the current

Given these developments, selling assets that circumstances it is easy to see why selling oil

have a higher carbon intensity could prove to be sands assets could be an attractive option for

an attractive strategy for the super-majors. And IOCs that have a variety of areas they can focus

while oil sands producers have made strides in on. If sales are announced, they will come as no

lowering the carbon intensity of their output, it great surprise.

Week 29 22•July•2021 www. NEWSBASE .com P5