Page 132 - Internal Auditing Standards

P. 132

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

In other cases, the link between pervasive and specific controls may be more direct. For example, some monitoring

controls may identify control breakdowns in specific (business process) controls. Testing these monitoring controls

for effectiveness might reduce (but not eliminate) the need for testing more specifi c controls.

Tests of pervasive controls (often referred to as entity-level and general IT controls) tend to be more subjective

(such as evaluating the commitment to integrity or competence), and therefore tend to be more diffi cult to

document than specific internal control at the business process level (such as checking to see if a payment

was authorized). As a result, the testing of entity-level and general IT controls is often documented with

memoranda to the file explaining the approach taken and the action steps (e.g., staff interviews, assessments,

review of employee files, etc.), along with supporting evidence.

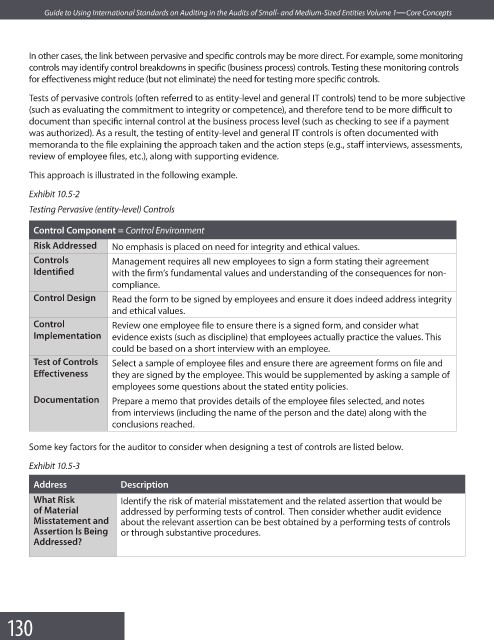

This approach is illustrated in the following example.

Exhibit 10.5-2

Testing Pervasive (entity-level) Controls

Control Component = Control Environment

Risk Addressed No emphasis is placed on need for integrity and ethical values.

Controls Management requires all new employees to sign a form stating their agreement

Identifi ed with the firm’s fundamental values and understanding of the consequences for non-

compliance.

Control Design Read the form to be signed by employees and ensure it does indeed address integrity

and ethical values.

Control Review one employee file to ensure there is a signed form, and consider what

Implementation evidence exists (such as discipline) that employees actually practice the values. This

could be based on a short interview with an employee.

Test of Controls Select a sample of employee files and ensure there are agreement forms on fi le and

Eff ectiveness they are signed by the employee. This would be supplemented by asking a sample of

employees some questions about the stated entity policies.

Documentation Prepare a memo that provides details of the employee files selected, and notes

from interviews (including the name of the person and the date) along with the

conclusions reached.

Some key factors for the auditor to consider when designing a test of controls are listed below.

Exhibit 10.5-3

Address Description

What Risk Identify the risk of material misstatement and the related assertion that would be

of Material addressed by performing tests of control. Then consider whether audit evidence

Misstatement and about the relevant assertion can be best obtained by a performing tests of controls

Assertion Is Being or through substantive procedures.

Addressed?

130