Page 131 - Internal Auditing Standards

P. 131

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

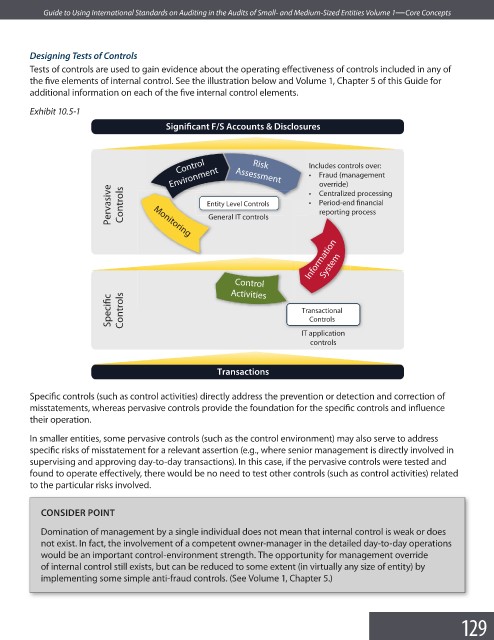

Designing Tests of Controls

Tests of controls are used to gain evidence about the operating effectiveness of controls included in any of

the five elements of internal control. See the illustration below and Volume 1, Chapter 5 of this Guide for

additional information on each of the five internal control elements.

Exhibit 10.5-1

Significant F/S Accounts & Disclosures

Control Risk Includes controls over:

Environment Assessment t Fraud (management

override)

Pervasive Controls Monitoring Entity Level Controlsls t Centralized processing

t Period-end financial

Leve

ty

Enti

l

Contro

reporting process

p

g

s

l

l

l

l

IT

t

con

IT

ro

t

General IT controls

G G

enera

Information

System

Control

Activities

Specific Controls Transactional

Controls

IT application

controls

Transactions

Specific controls (such as control activities) directly address the prevention or detection and correction of

misstatements, whereas pervasive controls provide the foundation for the specific controls and infl uence

their operation.

In smaller entities, some pervasive controls (such as the control environment) may also serve to address

specific risks of misstatement for a relevant assertion (e.g., where senior management is directly involved in

supervising and approving day-to-day transactions). In this case, if the pervasive controls were tested and

found to operate effectively, there would be no need to test other controls (such as control activities) related

to the particular risks involved.

CONSIDER POINT

Domination of management by a single individual does not mean that internal control is weak or does

not exist. In fact, the involvement of a competent owner-manager in the detailed day-to-day operations

would be an important control-environment strength. The opportunity for management override

of internal control still exists, but can be reduced to some extent (in virtually any size of entity) by

implementing some simple anti-fraud controls. (See Volume 1, Chapter 5.)

129