Page 126 - Internal Auditing Standards

P. 126

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Each technique has its particular strengths and weaknesses that the auditor needs to consider when

designing the analytical procedures. A complex technique such as regression analysis may provide statistically

reliable conclusions about a recorded amount. However, a simple technique such as multiplying the number

of apartments by the approved rental rates (per leases) and adjusting the result for actual vacancies may

provide a reliable and precise estimate of the rental revenue.

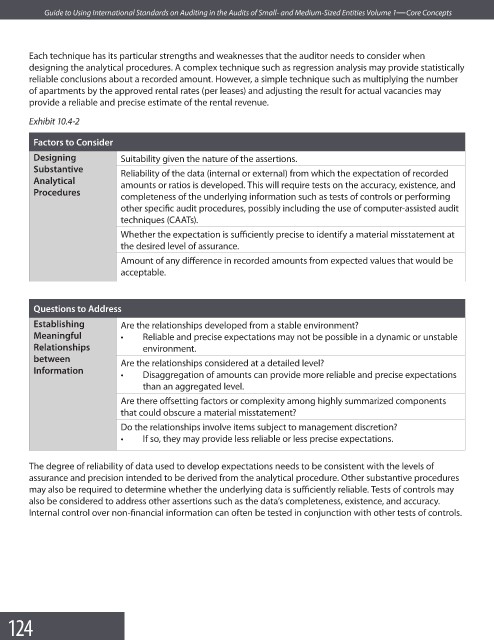

Exhibit 10.4-2

Factors to Consider

Designing Suitability given the nature of the assertions.

Substantive

Reliability of the data (internal or external) from which the expectation of recorded

Analytical amounts or ratios is developed. This will require tests on the accuracy, existence, and

Procedures

completeness of the underlying information such as tests of controls or performing

other specific audit procedures, possibly including the use of computer-assisted audit

techniques (CAATs).

Whether the expectation is sufficiently precise to identify a material misstatement at

the desired level of assurance.

Amount of any difference in recorded amounts from expected values that would be

acceptable.

Questions to Address

Establishing Are the relationships developed from a stable environment?

Meaningful • Reliable and precise expectations may not be possible in a dynamic or unstable

Relationships environment.

between

Are the relationships considered at a detailed level?

Information

• Disaggregation of amounts can provide more reliable and precise expectations

than an aggregated level.

Are there offsetting factors or complexity among highly summarized components

that could obscure a material misstatement?

Do the relationships involve items subject to management discretion?

• If so, they may provide less reliable or less precise expectations.

The degree of reliability of data used to develop expectations needs to be consistent with the levels of

assurance and precision intended to be derived from the analytical procedure. Other substantive procedures

may also be required to determine whether the underlying data is sufficiently reliable. Tests of controls may

also be considered to address other assertions such as the data’s completeness, existence, and accuracy.

Internal control over non-financial information can often be tested in conjunction with other tests of controls.

124