Page 125 - Internal Auditing Standards

P. 125

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

statements with an expectation developed from information obtained from understanding the entity, and

other audit evidence.

If the inherent risks are low for a class of transactions, substantive analytical procedures alone may provide

sufficient appropriate audit evidence. However, if the assessed risk is low because of related internal controls,

the auditor would also perform tests of those controls. Consequently for significant risks identifi ed, analytical

procedures would always be used in combination with other substantive tests or tests of control.

To use an analytical procedure as a substantive procedure, the auditor should design the procedure to

reduce the risk of not detecting a material misstatement in the relevant assertion to an acceptably low level.

This means that the expectation of what the recorded amount should be is precise enough to indicate the

possibility of a material misstatement, either individually or in the aggregate.

CONSIDER POINT

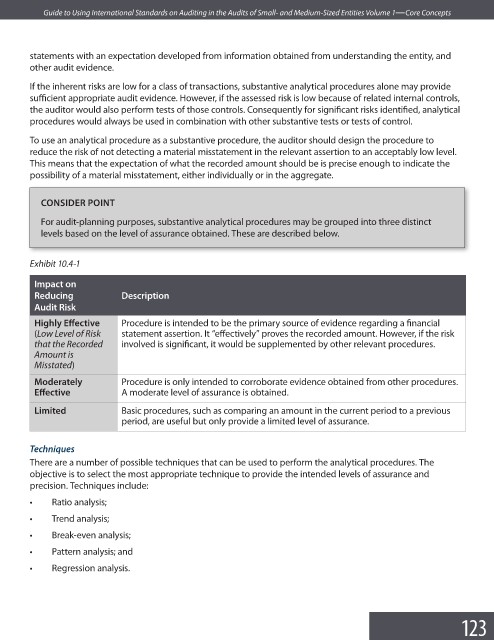

For audit-planning purposes, substantive analytical procedures may be grouped into three distinct

levels based on the level of assurance obtained. These are described below.

Exhibit 10.4-1

Impact on

Reducing Description

Audit Risk

Highly Eff ective Procedure is intended to be the primary source of evidence regarding a fi nancial

(Low Level of Risk statement assertion. It “effectively” proves the recorded amount. However, if the risk

that the Recorded involved is significant, it would be supplemented by other relevant procedures.

Amount is

Misstated)

Moderately Procedure is only intended to corroborate evidence obtained from other procedures.

Eff ective A moderate level of assurance is obtained.

Limited Basic procedures, such as comparing an amount in the current period to a previous

period, are useful but only provide a limited level of assurance.

Techniques

There are a number of possible techniques that can be used to perform the analytical procedures. The

objective is to select the most appropriate technique to provide the intended levels of assurance and

precision. Techniques include:

• Ratio analysis;

• Trend analysis;

• Break-even analysis;

• Pattern analysis; and

• Regression analysis.

123