Page 120 - Internal Auditing Standards

P. 120

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Tests of Details

When designing substantive procedures to respond to assessed risks, the auditor would consider a number of

matters, as set out below.

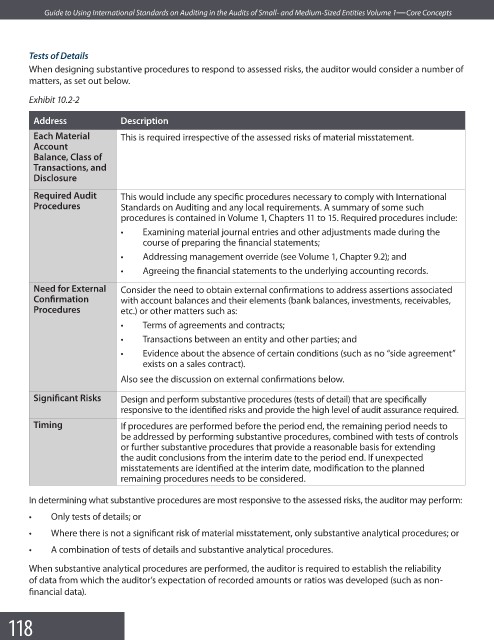

Exhibit 10.2-2

Address Description

Each Material This is required irrespective of the assessed risks of material misstatement.

Account

Balance, Class of

Transactions, and

Disclosure

Required Audit This would include any specific procedures necessary to comply with International

Procedures Standards on Auditing and any local requirements. A summary of some such

procedures is contained in Volume 1, Chapters 11 to 15. Required procedures include:

• Examining material journal entries and other adjustments made during the

course of preparing the fi nancial statements;

• Addressing management override (see Volume 1, Chapter 9.2); and

• Agreeing the financial statements to the underlying accounting records.

Need for External Consider the need to obtain external confirmations to address assertions associated

Confi rmation with account balances and their elements (bank balances, investments, receivables,

Procedures etc.) or other matters such as:

• Terms of agreements and contracts;

• Transactions between an entity and other parties; and

• Evidence about the absence of certain conditions (such as no “side agreement”

exists on a sales contract).

Also see the discussion on external confi rmations below.

Signifi cant Risks Design and perform substantive procedures (tests of detail) that are specifi cally

responsive to the identified risks and provide the high level of audit assurance required.

Timing If procedures are performed before the period end, the remaining period needs to

be addressed by performing substantive procedures, combined with tests of controls

or further substantive procedures that provide a reasonable basis for extending

the audit conclusions from the interim date to the period end. If unexpected

misstatements are identified at the interim date, modification to the planned

remaining procedures needs to be considered.

In determining what substantive procedures are most responsive to the assessed risks, the auditor may perform:

• Only tests of details; or

• Where there is not a significant risk of material misstatement, only substantive analytical procedures; or

• A combination of tests of details and substantive analytical procedures.

When substantive analytical procedures are performed, the auditor is required to establish the reliability

of data from which the auditor’s expectation of recorded amounts or ratios was developed (such as non-

fi nancial data).

118