Page 115 - Internal Auditing Standards

P. 115

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

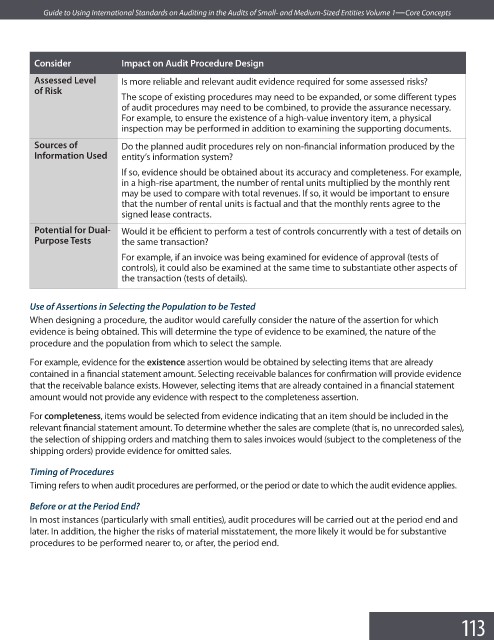

Consider Impact on Audit Procedure Design

Assessed Level Is more reliable and relevant audit evidence required for some assessed risks?

of Risk

The scope of existing procedures may need to be expanded, or some diff erent types

of audit procedures may need to be combined, to provide the assurance necessary.

For example, to ensure the existence of a high-value inventory item, a physical

inspection may be performed in addition to examining the supporting documents.

Sources of Do the planned audit procedures rely on non-financial information produced by the

Information Used entity’s information system?

If so, evidence should be obtained about its accuracy and completeness. For example,

in a high-rise apartment, the number of rental units multiplied by the monthly rent

may be used to compare with total revenues. If so, it would be important to ensure

that the number of rental units is factual and that the monthly rents agree to the

signed lease contracts.

Potential for Dual- Would it be efficient to perform a test of controls concurrently with a test of details on

Purpose Tests the same transaction?

For example, if an invoice was being examined for evidence of approval (tests of

controls), it could also be examined at the same time to substantiate other aspects of

the transaction (tests of details).

Use of Assertions in Selecting the Population to be Tested

When designing a procedure, the auditor would carefully consider the nature of the assertion for which

evidence is being obtained. This will determine the type of evidence to be examined, the nature of the

procedure and the population from which to select the sample.

For example, evidence for the existence assertion would be obtained by selecting items that are already

contained in a financial statement amount. Selecting receivable balances for confirmation will provide evidence

that the receivable balance exists. However, selecting items that are already contained in a fi nancial statement

amount would not provide any evidence with respect to the completeness assertion.

For completeness, items would be selected from evidence indicating that an item should be included in the

relevant financial statement amount. To determine whether the sales are complete (that is, no unrecorded sales),

the selection of shipping orders and matching them to sales invoices would (subject to the completeness of the

shipping orders) provide evidence for omitted sales.

Timing of Procedures

Timing refers to when audit procedures are performed, or the period or date to which the audit evidence applies.

Before or at the Period End?

In most instances (particularly with small entities), audit procedures will be carried out at the period end and

later. In addition, the higher the risks of material misstatement, the more likely it would be for substantive

procedures to be performed nearer to, or after, the period end.

113