Page 110 - Internal Auditing Standards

P. 110

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

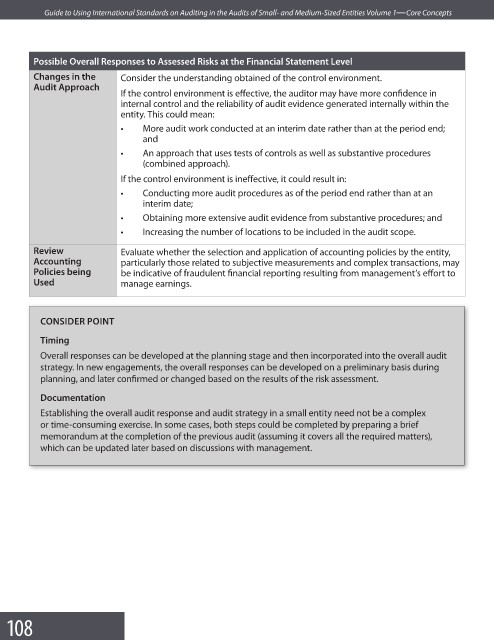

Possible Overall Responses to Assessed Risks at the Financial Statement Level

Changes in the Consider the understanding obtained of the control environment.

Audit Approach

If the control environment is effective, the auditor may have more confi dence in

internal control and the reliability of audit evidence generated internally within the

entity. This could mean:

• More audit work conducted at an interim date rather than at the period end;

and

• An approach that uses tests of controls as well as substantive procedures

(combined approach).

If the control environment is ineffective, it could result in:

• Conducting more audit procedures as of the period end rather than at an

interim date;

• Obtaining more extensive audit evidence from substantive procedures; and

• Increasing the number of locations to be included in the audit scope.

Review Evaluate whether the selection and application of accounting policies by the entity,

Accounting particularly those related to subjective measurements and complex transactions, may

Policies being be indicative of fraudulent financial reporting resulting from management’s eff ort to

Used manage earnings.

CONSIDER POINT

Timing

Overall responses can be developed at the planning stage and then incorporated into the overall audit

strategy. In new engagements, the overall responses can be developed on a preliminary basis during

planning, and later confirmed or changed based on the results of the risk assessment.

Documentation

Establishing the overall audit response and audit strategy in a small entity need not be a complex

or time-consuming exercise. In some cases, both steps could be completed by preparing a brief

memorandum at the completion of the previous audit (assuming it covers all the required matters),

which can be updated later based on discussions with management.

108