Page 108 - Internal Auditing Standards

P. 108

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

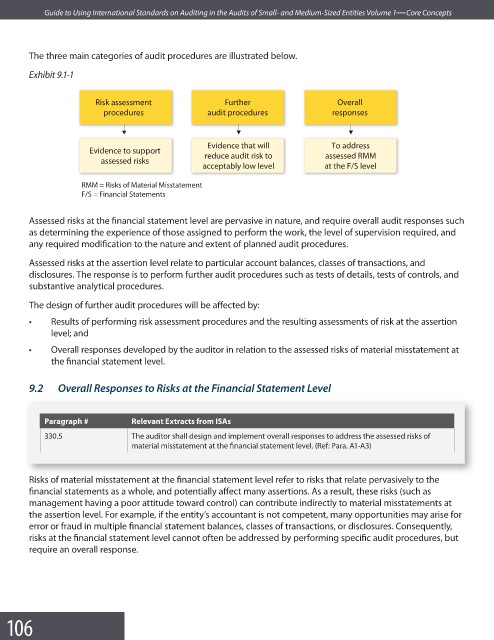

The three main categories of audit procedures are illustrated below.

Exhibit 9.1-1

Risk assessment Further Overall

procedures audit procedures responses

Evidence that will To address

Evidence to support

reduce audit risk to assessed RMM

assessed risks

acceptably low level at the F/S level

RMM = Risks of Material Misstatement

F/S = Financial Statements

Assessed risks at the financial statement level are pervasive in nature, and require overall audit responses such

as determining the experience of those assigned to perform the work, the level of supervision required, and

any required modification to the nature and extent of planned audit procedures.

Assessed risks at the assertion level relate to particular account balances, classes of transactions, and

disclosures. The response is to perform further audit procedures such as tests of details, tests of controls, and

substantive analytical procedures.

The design of further audit procedures will be aff ected by:

• Results of performing risk assessment procedures and the resulting assessments of risk at the assertion

level; and

• Overall responses developed by the auditor in relation to the assessed risks of material misstatement at

the financial statement level.

9.2 Overall Responses to Risks at the Financial Statement Level

Paragraph # Relevant Extracts from ISAs

330.5 The auditor shall design and implement overall responses to address the assessed risks of

material misstatement at the financial statement level. (Ref: Para. A1-A3)

Risks of material misstatement at the financial statement level refer to risks that relate pervasively to the

financial statements as a whole, and potentially affect many assertions. As a result, these risks (such as

management having a poor attitude toward control) can contribute indirectly to material misstatements at

the assertion level. For example, if the entity’s accountant is not competent, many opportunities may arise for

error or fraud in multiple financial statement balances, classes of transactions, or disclosures. Consequently,

risks at the financial statement level cannot often be addressed by performing specific audit procedures, but

require an overall response.

106