Page 105 - Internal Auditing Standards

P. 105

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

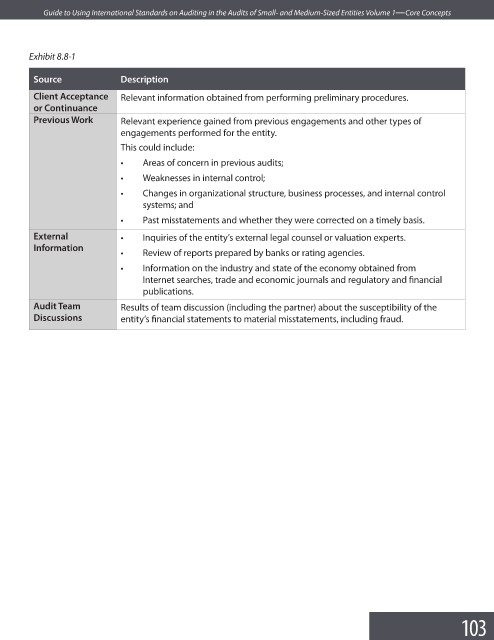

Exhibit 8.8-1

Source Description

Client Acceptance Relevant information obtained from performing preliminary procedures.

or Continuance

Previous Work Relevant experience gained from previous engagements and other types of

engagements performed for the entity.

This could include:

• Areas of concern in previous audits;

• Weaknesses in internal control;

• Changes in organizational structure, business processes, and internal control

systems; and

• Past misstatements and whether they were corrected on a timely basis.

External • Inquiries of the entity’s external legal counsel or valuation experts.

Information

• Review of reports prepared by banks or rating agencies.

• Information on the industry and state of the economy obtained from

Internet searches, trade and economic journals and regulatory and fi nancial

publications.

Audit Team Results of team discussion (including the partner) about the susceptibility of the

Discussions entity’s financial statements to material misstatements, including fraud.

103