Page 107 - Internal Auditing Standards

P. 107

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Paragraph # Relevant Extracts from ISAs

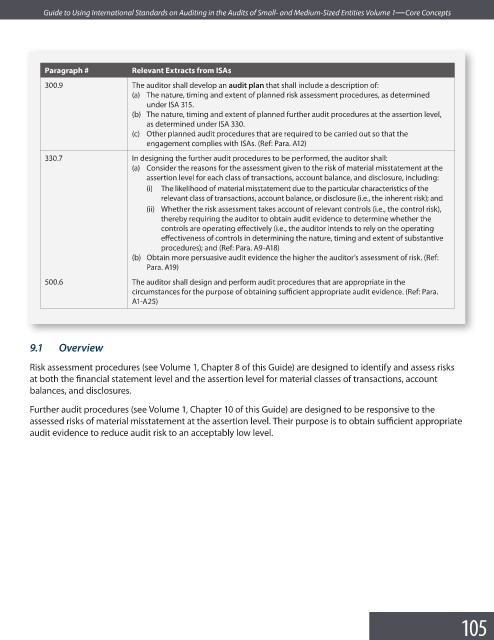

300.9 The auditor shall develop an audit plan that shall include a description of:

(a) The nature, timing and extent of planned risk assessment procedures, as determined

under ISA 315.

(b) The nature, timing and extent of planned further audit procedures at the assertion level,

as determined under ISA 330.

(c) Other planned audit procedures that are required to be carried out so that the

engagement complies with ISAs. (Ref: Para. A12)

330.7 In designing the further audit procedures to be performed, the auditor shall:

(a) Consider the reasons for the assessment given to the risk of material misstatement at the

assertion level for each class of transactions, account balance, and disclosure, including:

(i) The likelihood of material misstatement due to the particular characteristics of the

relevant class of transactions, account balance, or disclosure (i.e., the inherent risk); and

(ii) Whether the risk assessment takes account of relevant controls (i.e., the control risk),

thereby requiring the auditor to obtain audit evidence to determine whether the

controls are operating effectively (i.e., the auditor intends to rely on the operating

effectiveness of controls in determining the nature, timing and extent of substantive

procedures); and (Ref: Para. A9-A18)

(b) Obtain more persuasive audit evidence the higher the auditor’s assessment of risk. (Ref:

Para. A19)

500.6 The auditor shall design and perform audit procedures that are appropriate in the

circumstances for the purpose of obtaining sufficient appropriate audit evidence. (Ref: Para.

A1-A25)

9.1 Overview

Risk assessment procedures (see Volume 1, Chapter 8 of this Guide) are designed to identify and assess risks

at both the financial statement level and the assertion level for material classes of transactions, account

balances, and disclosures.

Further audit procedures (see Volume 1, Chapter 10 of this Guide) are designed to be responsive to the

assessed risks of material misstatement at the assertion level. Their purpose is to obtain suffi cient appropriate

audit evidence to reduce audit risk to an acceptably low level.

105