Page 113 - Internal Auditing Standards

P. 113

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

9.3 Response to Assessed Risks at the Assertion Level

Paragraph # Relevant Extracts from ISAs

330.6 The auditor shall design and perform further audit procedures whose nature, timing and

extent are based on and are responsive to the assessed risks of material misstatement at the

assertion level. (Ref: Para. A4-A8)

The auditor’s assessment of identified risks at the assertion level provides the starting point for:

• Considering the appropriate audit approach; and

• Designing and performing further audit procedures. Refer to Volume 1, Chapter 10 for a detailed

description of further audit procedures.

An Appropriate Audit Approach

The audit approach for designing and performing further audit procedures will be based on the assessment

of the identified risks at both the financial statement level and the assertion level.

Because assessed risks will differ between the material classes of transactions, account balances, and

disclosures, the most effective audit approach will vary. For example, it might be appropriate to test controls

over sales completeness, and use substantive procedures for the other assertions. For payables, a substantive

approach could be applicable for all assertions. The key is to develop audit procedures that respond

appropriately to the risks identifi ed.

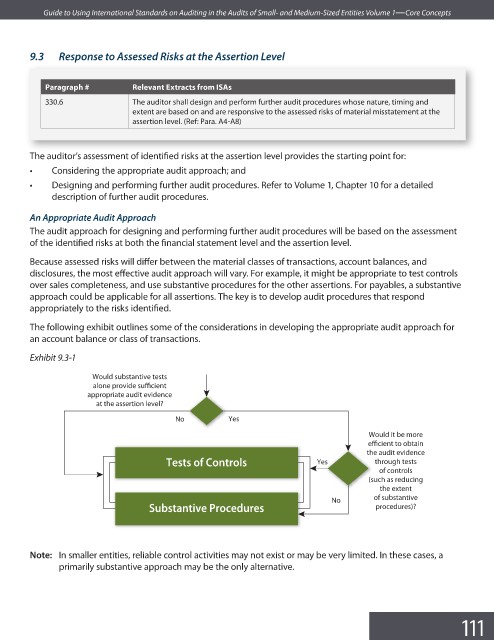

The following exhibit outlines some of the considerations in developing the appropriate audit approach for

an account balance or class of transactions.

Exhibit 9.3-1

Would substantive tests

alone provide sufficient

appropriate audit evidence

at the assertion level?

No Yes

W

Would it be more

efficient to obtain

effi

the

the audit evidence

r

t

l

o

n

ts

Tests of Controlss Yes through tests

o

Co

f

of controls

(s

(such as reducing

the extent

No of substantive

Substantive Procedures procedures)?

Note: In smaller entities, reliable control activities may not exist or may be very limited. In these cases, a

primarily substantive approach may be the only alternative.

111