Page 20 - Internal Auditing Standards

P. 20

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

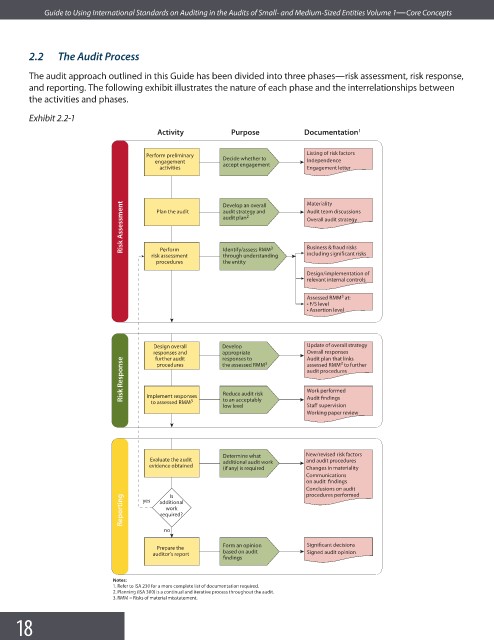

2.2 The Audit Process

The audit approach outlined in this Guide has been divided into three phases—risk assessment, risk response,

and reporting. The following exhibit illustrates the nature of each phase and the interrelationships between

the activities and phases.

Exhibit 2.2-1

Activity Purpose Documentation 1

Listing of risk factors

Perform preliminary Decide whether to

engagement accept engagement Independence

activities Engagement letter

Risk Assessment Plan the audit Develop an overall Materiality

Audit team discussions

audit strategy and

2

audit plan

Overall audit strategy

Perform

including significant risks

risk assessment Identify/assess RMM 3 Business & fraud risks

through understanding

procedures the entity

Design/implementation of

relevant internal controls

3

Assessed RMM at:

t F/S level

t Assertion level

Design overall Develop Update of overall strategy

responses and appropriate 3 Overall responses

Audit plan that links

responses to

further audit

Risk Response audit procedures

3

the assessed RMM

assessed RMM to further

procedures

Work performed

Implement responses

to an acceptably

to assessed RMM 3 Reduce audit risk Audit findings

low level Staff supervision

Working paper review

Determine what New/revised risk factors

Evaluate the audit additional audit work and audit procedures

evidence obtained

(if any) is required Changes in materiality

Communications

on audit findings

Conclusions on audit

procedures performed

Is

Reporting yes additional

work

required?

no

Form an opinion Significant decisions

Prepare the

auditor’s report based on audit Signed audit opinion

findings

Notes:

1. Refer to ISA 230 for a more complete list of documentation required.

2. Planning (ISA 300) is a continual and iterative process throughout the audit.

3. RMM = Risks of material misstatement.

18