Page 25 - Internal Auditing Standards

P. 25

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Scope of an Audit

The scope of the auditor’s work and the opinion provided are usually confined to whether the fi nancial

statements are prepared, in all material respects, in accordance with the applicable fi nancial reporting

framework. As a result, an unmodified auditor’s report does not provide any assurance about the future viability

of the entity, nor the effi ciency or effectiveness with which management has conducted the affairs of the entity.

Any extension of this basic audit responsibility, such as that required by local laws or securities regulations,

would require the auditor to undertake further work and to modify or expand the auditor’s report

accordingly.

Material Misstatements

A material misstatement (the aggregate of all uncorrected misstatements and missing/misleading disclosures

in the financial statements, including omissions) has occurred when they could reasonably be expected to

influence the economic decisions of users made on the basis of the fi nancial statements.

Assertions

Assertions are representations by management, explicit or otherwise, that are embodied in the fi nancial

statements. They relate to the recognition, measurement, presentation, and disclosure of the various

elements (amounts and disclosures) in the financial statements. For example, the completeness assertion

relates to all transactions and events that should have been recorded having been recorded. They are used

by the auditor to consider the different types of potential misstatements that may occur.

3.2 Audit Risk

Audit risk is the risk of expressing an inappropriate audit opinion on financial statements that are materially

misstated. The objective of the audit is to reduce this audit risk to an acceptably low level.

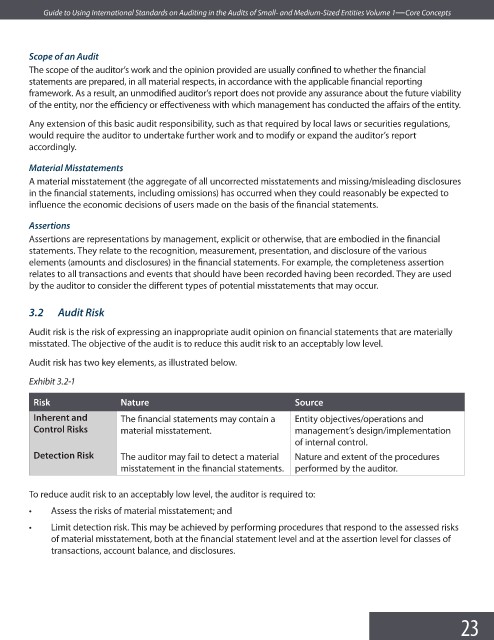

Audit risk has two key elements, as illustrated below.

Exhibit 3.2-1

Risk Nature Source

Inherent and The financial statements may contain a Entity objectives/operations and

Control Risks material misstatement. management’s design/implementation

of internal control.

Detection Risk The auditor may fail to detect a material Nature and extent of the procedures

misstatement in the fi nancial statements. performed by the auditor.

To reduce audit risk to an acceptably low level, the auditor is required to:

• Assess the risks of material misstatement; and

• Limit detection risk. This may be achieved by performing procedures that respond to the assessed risks

of material misstatement, both at the financial statement level and at the assertion level for classes of

transactions, account balance, and disclosures.

23