Page 34 - Internal Auditing Standards

P. 34

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

p

g

Reporting

Paragraph # ISA Objective(s)

700.6 The objectives of the auditor are:

(a) To form an opinion on the financial statements based on an evaluation of the conclusions

drawn from the audit evidence obtained; and

(b) To express clearly that opinion through a written report that also describes the basis for

that opinion.

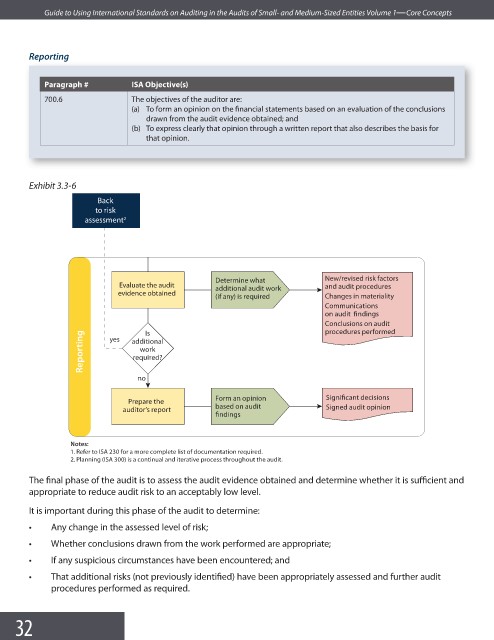

Exhibit 3.3-6

Back

to risk

assessment 2

Determine what New/revised risk factors

Evaluate the audit additional audit work and audit procedures

evidence obtained

(if any) is required Changes in materiality

Communications

on audit findings

Conclusions on audit

procedures performed

Is

Reporting yes additional

work

required?

no

Form an opinion Significant decisions

Prepare the

auditor’s report based on audit Signed audit opinion

findings

Notes:

1. Refer to ISA 230 for a more complete list of documentation required.

2. Planning (ISA 300) is a continual and iterative process throughout the audit.

The final phase of the audit is to assess the audit evidence obtained and determine whether it is suffi cient and

appropriate to reduce audit risk to an acceptably low level.

It is important during this phase of the audit to determine:

• Any change in the assessed level of risk;

• Whether conclusions drawn from the work performed are appropriate;

• If any suspicious circumstances have been encountered; and

• That additional risks (not previously identified) have been appropriately assessed and further audit

procedures performed as required.

32