Page 32 - Internal Auditing Standards

P. 32

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Requirements Description

Use of Professional The ISA audit requirements require the use and then documentation of signifi cant

Judgment judgments made by the auditor throughout the audit. Typical examples of tasks

throughout the risk assessment process include:

• Deciding to accept or continue with the client;

• Developing the overall audit strategy;

• Establishing materiality;

• Assessing risks of material misstatement, including the identification of signifi cant

risks and other areas where special audit consideration may be necessary; and

• Developing expectations for use when performing analytical procedures.

Risk Response

Paragraph # ISA Objective(s)

330.3 The objective of the auditor is to obtain sufficient appropriate audit evidence regarding the

assessed risks of material misstatement, through designing and implementing appropriate

responses to those risks.

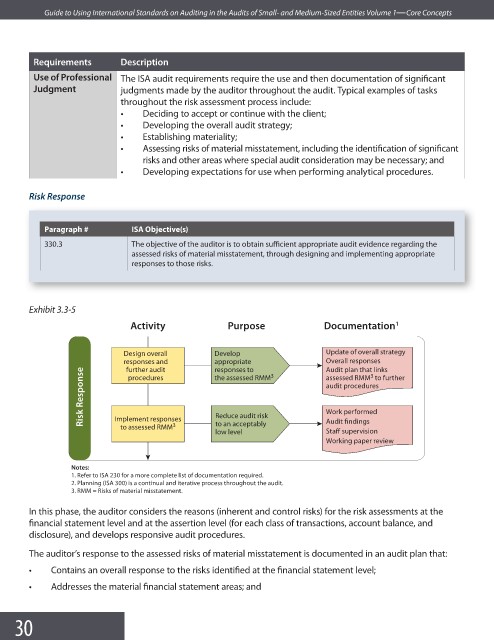

Exhibit 3.3-5

Activity Purpose Documentation 1

Design overall Develop Update of overall strategy

responses and appropriate 3 Overall responses

further audit

responses to

Audit plan that links

Risk Response audit procedures

3

assessed RMM to further

procedures

the assessed RMM

Work performed

Reduce audit risk

Implement responses

to an acceptably

3

to assessed RMM

Staff supervision

low level Audit findings

Working paper review

Notes:

1. Refer to ISA 230 for a more complete list of documentation required.

2. Planning (ISA 300) is a continual and iterative process throughout the audit.

3. RMM = Risks of material misstatement.

In this phase, the auditor considers the reasons (inherent and control risks) for the risk assessments at the

financial statement level and at the assertion level (for each class of transactions, account balance, and

disclosure), and develops responsive audit procedures.

The auditor’s response to the assessed risks of material misstatement is documented in an audit plan that:

• Contains an overall response to the risks identified at the financial statement level;

• Addresses the material financial statement areas; and

30