Page 40 - Internal Auditing Standards

P. 40

4. Ethics, ISAs, and Quality Control

Chapter Content Relevant ISAs

Matters to be addressed in a firm’s system of quality control to ensure

compliance with ethical (including independence) requirements and ISQC 1, 200, 220

the ISAs.

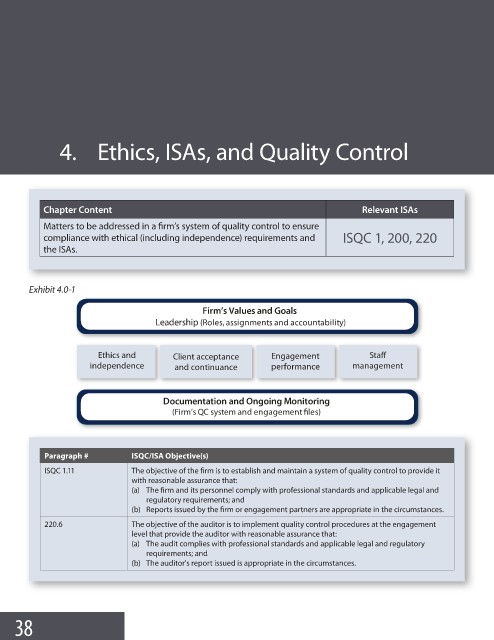

Exhibit 4.0-1

Firm’s Values and Goals

Leadership (Roles, assignments and accountability)

Ethics and Client acceptance Engagement Staff

independence and continuance performance management

Documentation and Ongoing Monitoring

(Firm’s QC system and engagement files)

Paragraph # ISQC/ISA Objective(s)

ISQC 1.11 The objective of the firm is to establish and maintain a system of quality control to provide it

with reasonable assurance that:

(a) The firm and its personnel comply with professional standards and applicable legal and

regulatory requirements; and

(b) Reports issued by the firm or engagement partners are appropriate in the circumstances.

220.6 The objective of the auditor is to implement quality control procedures at the engagement

level that provide the auditor with reasonable assurance that:

(a) The audit complies with professional standards and applicable legal and regulatory

requirements; and

(b) The auditor's report issued is appropriate in the circumstances.

38