Page 35 - 2019-20 CAFR

P. 35

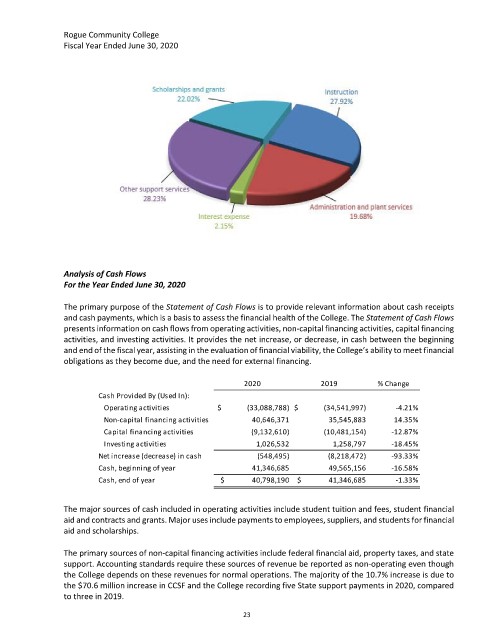

Rogue Community College

Fiscal Year Ended June 30, 2020

Analysis of Cash Flows

For the Year Ended June 30, 2020

The primary purpose of the Statement of Cash Flows is to provide relevant information about cash receipts

and cash payments, which is a basis to assess the financial health of the College. The Statement of Cash Flows

presents information on cash flows from operating activities, non-capital financing activities, capital financing

activities, and investing activities. It provides the net increase, or decrease, in cash between the beginning

and end of the fiscal year, assisting in the evaluation of financial viability, the College’s ability to meet financial

obligations as they become due, and the need for external financing.

2020 2019 % Change

Cash Provided By (Used In):

Operating activities $ (33,088,788) $ (34,541,997) -4.21%

Non-capital financing activities 40,646,371 35,545,883 14.35%

Capital financing activities (9,132,610) (10,481,154) -12.87%

Investing activities 1,026,532 1,258,797 -18.45%

Net increase (decrease) in cash (548,495) (8,218,472) -93.33%

Cash, beginning of year 41,346,685 49,565,156 -16.58%

Cash, end of year $ 40,798,190 $ 41,346,685 -1.33%

The major sources of cash included in operating activities include student tuition and fees, student financial

aid and contracts and grants. Major uses include payments to employees, suppliers, and students for financial

aid and scholarships.

The primary sources of non-capital financing activities include federal financial aid, property taxes, and state

support. Accounting standards require these sources of revenue be reported as non-operating even though

the College depends on these revenues for normal operations. The majority of the 10.7% increase is due to

the $70.6 million increase in CCSF and the College recording five State support payments in 2020, compared

to three in 2019.

23