Page 253 - BA2 Integrated Workbook - Student 2017

P. 253

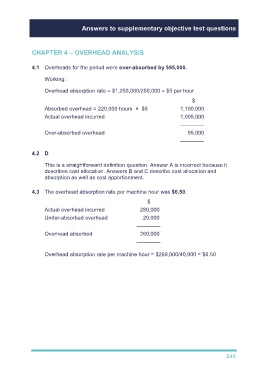

Answers to supplementary objective test questions

CHAPTER 4 – OVERHEAD ANALYSIS

4.1 Overheads for the period were over-absorbed by $95,000.

Working:

Overhead absorption rate = $1,250,000/250,000 = $5 per hour

$

Absorbed overhead = 220,000 hours × $5 1,100,000

Actual overhead incurred 1,005,000

––––––––

Over-absorbed overhead 95,000

––––––––

4.2 D

This is a straightforward definition question. Answer A is incorrect because it

describes cost allocation. Answers B and C describe cost allocation and

absorption as well as cost apportionment.

4.3 The overhead absorption rate per machine hour was $6.50.

$

Actual overhead incurred 280,000

Under-absorbed overhead 20,000

––––––––

Overhead absorbed 260,000

––––––––

Overhead absorption rate per machine hour = $260,000/40,000 = $6.50

245