Page 257 - BA2 Integrated Workbook - Student 2017

P. 257

Answers to supplementary objective test questions

CHAPTER 8 – INTEGRATED ACCOUNTING SYSTEMS

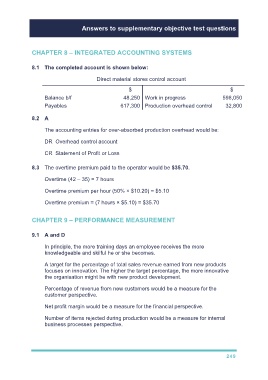

8.1 The completed account is shown below:

Direct material stores control account

$ $

Balance b/f 48,250 Work in progress 598,050

Payables 617,300 Production overhead control 32,800

8.2 A

The accounting entries for over-absorbed production overhead would be:

DR Overhead control account

CR Statement of Profit or Loss

8.3 The overtime premium paid to the operator would be $35.70.

Overtime (42 – 35) = 7 hours

Overtime premium per hour (50% × $10.20) = $5.10

Overtime premium = (7 hours × $5.10) = $35.70

CHAPTER 9 – PERFORMANCE MEASUREMENT

9.1 A and D

In principle, the more training days an employee receives the more

knowledgeable and skilful he or she becomes.

A target for the percentage of total sales revenue earned from new products

focuses on innovation. The higher the target percentage, the more innovative

the organisation might be with new product development.

Percentage of revenue from new customers would be a measure for the

customer perspective.

Net profit margin would be a measure for the financial perspective.

Number of items rejected during production would be a measure for internal

business processes perspective.

249