Page 256 - BA2 Integrated Workbook - Student 2017

P. 256

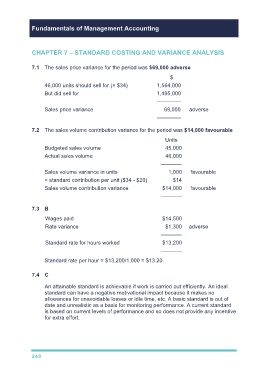

Fundamentals of Management Accounting

CHAPTER 7 – STANDARD COSTING AND VARIANCE ANALYSIS

7.1 The sales price variance for the period was $69,000 adverse

$

46,000 units should sell for (× $34) 1,564,000

But did sell for 1,495,000

––––––––

Sales price variance 69,000 adverse

––––––––

7.2 The sales volume contribution variance for the period was $14,000 favourable

Units

Budgeted sales volume 45,000

Actual sales volume 46,000

–––––––

Sales volume variance in units 1,000 favourable

× standard contribution per unit ($34 - $20) $14

Sales volume contribution variance $14,000 favourable

–––––––

7.3 B

Wages paid $14,500

Rate variance $1,300 adverse

–––––––

Standard rate for hours worked $13,200

–––––––

Standard rate per hour = $13,200/1,000 = $13.20.

7.4 C

An attainable standard is achievable if work is carried out efficiently. An ideal

standard can have a negative motivational impact because it makes no

allowances for unavoidable losses or idle time, etc. A basic standard is out of

date and unrealistic as a basis for monitoring performance. A current standard

is based on current levels of performance and so does not provide any incentive

for extra effort.

248