Page 10 - FINAL CFA SLIDES DECEMBER 2018 DAY 15

P. 10

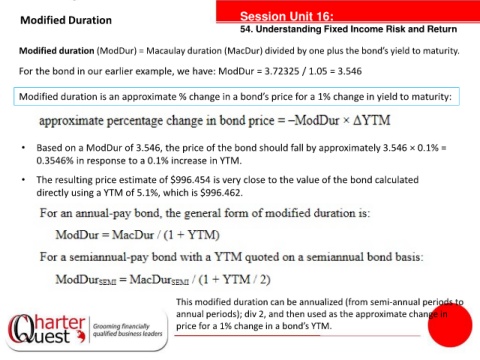

Modified Duration Session Unit 16:

54. Understanding Fixed Income Risk and Return

Modified duration (ModDur) = Macaulay duration (MacDur) divided by one plus the bond’s yield to maturity.

For the bond in our earlier example, we have: ModDur = 3.72325 / 1.05 = 3.546

Modified duration is an approximate % change in a bond’s price for a 1% change in yield to maturity:

tanties

• Based on a ModDur of 3.546, the price of the bond should fall by approximately 3.546 × 0.1% =

0.3546% in response to a 0.1% increase in YTM.

• The resulting price estimate of $996.454 is very close to the value of the bond calculated

directly using a YTM of 5.1%, which is $996.462.

This modified duration can be annualized (from semi-annual periods to

annual periods); div 2, and then used as the approximate change in

price for a 1% change in a bond’s YTM.