Page 264 - Microsoft Word - 00 IWB ACCA F7.docx

P. 264

Chapter 21

Liquidity

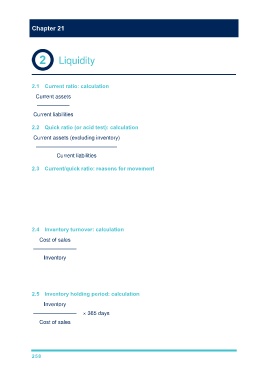

2.1 Current ratio: calculation

Current assets

——————

Current liabilities

2.2 Quick ratio (or acid test): calculation

Current assets (excluding inventory)

———————————————

Current liabilities

2.3 Current/quick ratio: reasons for movement

increase/decrease in cash balance

increase/decrease in inventory

increase/decrease in receivables

increase/decrease in payables

2.4 Inventory turnover: calculation

Cost of sales

————————

Inventory

number of times inventory is turned over in the period

higher turnover = higher efficiency

2.5 Inventory holding period: calculation

Inventory

———————— × 365 days

Cost of sales

average number of days for which inventory held

lower days = higher efficiency

258