Page 421 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 421

Answers

CHAPTER 13 – BASIC GROP ACCOUNTS – GOODWILL AND JOINT

ARRANGEMENTS

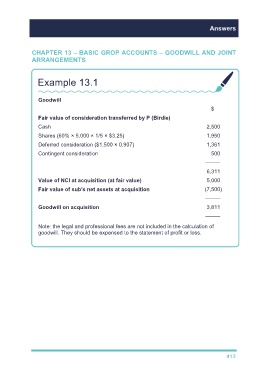

Example 13.1

Goodwill

$

Fair value of consideration transferred by P (Birdie)

Cash 2,500

Shares (60% × 5,000 × 1/5 × $3.25) 1,950

Deferred consideration ($1,500 × 0.907) 1,361

Contingent consideration 500

–––––

6,311

Value of NCI at acquisition (at fair value) 5,000

Fair value of sub's net assets at acquisition (7,500)

–––––

Goodwill on acquisition 3,811

–––––

Note: the legal and professional fees are not included in the calculation of

goodwill. They should be expensed to the statement of profit or loss.

413