Page 517 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 517

Answers to supplementary objective test questions

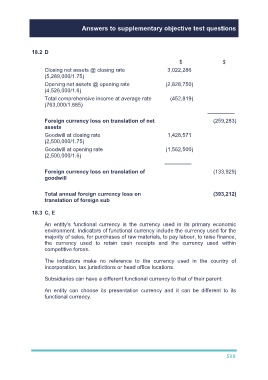

18.2 D

$ $

Closing net assets @ closing rate 3,022,286

(5,289,000/1.75)

Opening net assets @ opening rate (2,828,750)

(4.526,000/1.6)

Total comprehensive income at average rate (452,819)

(763,000/1.685)

–––––––––

Foreign currency loss on translation of net (259,283)

assets

Goodwill at closing rate 1,428,571

(2,500,000/1.75)

Goodwill at opening rate (1,562,500)

(2,500,000/1.6)

–––––––––

Foreign currency loss on translation of (133,929)

goodwill

Total annual foreign currency loss on (393,212)

translation of foreign sub

18.3 C, E

An entity’s functional currency is the currency used in its primary economic

environment. Indicators of functional currency include the currency used for the

majority of sales, for purchases of raw materials, to pay labour, to raise finance,

the currency used to retain cash receipts and the currency used within

competitive forces.

The indicators make no reference to the currency used in the country of

incorporation, tax jurisdictions or head office locations.

Subsidiaries can have a different functional currency to that of their parent.

An entity can choose its presentation currency and it can be different to its

functional currency.

509