Page 513 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 513

Answers to supplementary objective test questions

16.3 C, E and F

Dividends received are not shown separately within the statement of changes in

equity. Dividends paid by the parent and the dividends paid by the subsidiary to

non-controlling interests are recorded separately but not dividends received.

Only share capital and share premium of the parent is included. The

subsidiary’s share capital and share premium are not shown within the

consolidated financial statements at all.

Revaluation gains for the group will be shown within the consolidated statement

of changes in equity as part of the total comprehensive income for the year

attributable to P and NCI’s.

CHAPTER 17 – CONSOLIDATED STATEMENT OF CASH FLOW

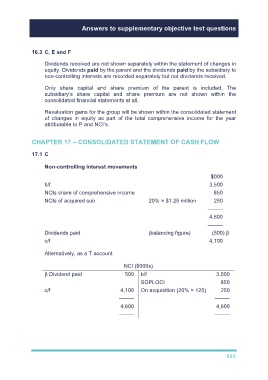

17.1 C

Non-controlling interest movements

$000

b/f 3,500

NCIs share of comprehensive income 850

NCIs of acquired sub 20% × $1.25 million 250

–––––

4,600

–––––

Dividends paid (balancing figure) (500) β

c/f 4,100

Alternatively, as a T account

NCI ($000s)

β Dividend paid 500 b/f 3,500

SOPLOCI 850

c/f 4,100 On acquisition (20% × 125) 250

––––– –––––

4,600 4,600

––––– –––––

505