Page 510 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 510

F2: Advanced Financial Reporting

15.2 D

The scenario described a control to control step-acquisition. The transaction is

treated as if the parent has paid cash to reduce the non-controlling interest. Any

difference between cash would be taken to equity as a transfer between

shareholders. The following double entry is posted:

Dr NCI 700,000 ($1,400,000 × 15/30)

Cr Cash $610,000

Cr Equity $90,000

The entry to equity is a credit and not debit, therefore D is incorrect.

The shareholding of 70% is increased to 85% on the 1st March 20X6. Ho is a

subsidiary for the entire period of the year ended 31st December 20X6. NCI’s

share of profits must be pro-rated in the statement of profit or loss to reflect

percentages before and after the acquisition. The NCI% is 30% before the step-

acquisition and 15% after.

The remaining options regarding the statement of financial position and goodwill

are correct.

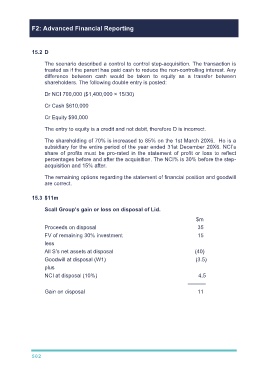

15.3 $11m

Scall Group’s gain or loss on disposal of Lid.

$m

Proceeds on disposal 35

FV of remaining 30% investment 15

less

All S’s net assets at disposal (40)

Goodwill at disposal (W1) (3.5)

plus

NCI at disposal (10%) 4.5

––––––

Gain on disposal 11

502