Page 7 - FINAL CFA II SLIDES JUNE 2019 DAY 9

P. 7

LOS 34.b: Describe the forward pricing and forward

rate models and calculate forward and spot prices READING 34: THE TERM STRUCTURE AND

and rates using those models. INTEREST RATE DYNAMICS

MODULE 34.1: SPOT AND FORWARD RATES, PART 1

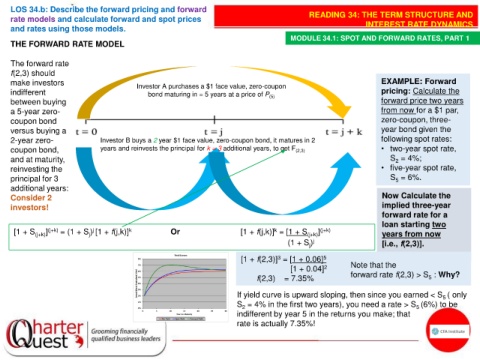

THE FORWARD RATE MODEL

The forward rate

f(2,3) should

make investors Investor A purchases a $1 face value, zero-coupon EXAMPLE: Forward

indifferent bond maturing in = 5 years at a price of P (5) pricing: Calculate the

between buying forward price two years

a 5-year zero- from now for a $1 par,

coupon bond zero-coupon, three-

versus buying a year bond given the

2-year zero- Investor B buys a 2 year $1 face value, zero-coupon bond, it matures in 2 following spot rates:

coupon bond, years and reinvests the principal for k = 3 additional years, to get F (2,3) • two-year spot rate,

and at maturity, S = 4%;

2

reinvesting the • five-year spot rate,

principal for 3 S = 6%.

5

additional years:

Consider 2 Now Calculate the

investors! implied three-year

forward rate for a

loan starting two

k

[1 + S (j+k) ] (j+k) = (1 + S ) [1 + f(j,k)] k Or [1 + f(j,k)] = [1 + S (j+k) ] (j+k) years from now

j

j

(1 + S ) j [i.e., f(2,3)].

j

[1 + f(2,3)] = [1 + 0.06] 5

3

[1 + 0.04] 2 Note that the

f(2,3) = 7.35% forward rate f(2,3) > S : Why?

5

If yield curve is upward sloping, then since you earned < S ( only

5

S = 4% in the first two years), you need a rate > S (6%) to be

5

2

indifferent by year 5 in the returns you make; that

rate is actually 7.35%!