Page 41 - PowerPoint Presentation

P. 41

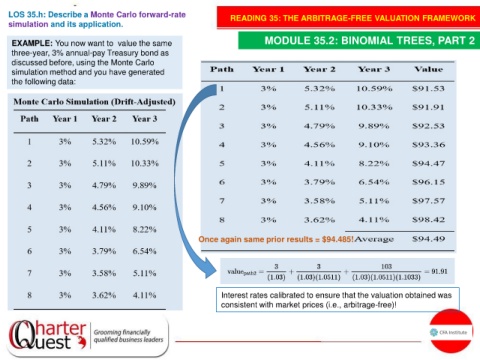

LOS 35.h: Describe a Monte Carlo forward-rate READING 35: THE ARBITRAGE-FREE VALUATION FRAMEWORK

simulation and its application.

EXAMPLE: You now want to value the same MODULE 35.2: BINOMIAL TREES, PART 2

three-year, 3% annual-pay Treasury bond as

discussed before, using the Monte Carlo

simulation method and you have generated

the following data:

Once again same prior results = $94.485!

Interest rates calibrated to ensure that the valuation obtained was

consistent with market prices (i.e., arbitrage-free)!