Page 40 - PowerPoint Presentation

P. 40

LOS 35.h: Describe a Monte Carlo forward-rate READING 35: THE ARBITRAGE-FREE VALUATION FRAMEWORK

simulation and its application.

MODULE 35.2: BINOMIAL TREES, PART 2

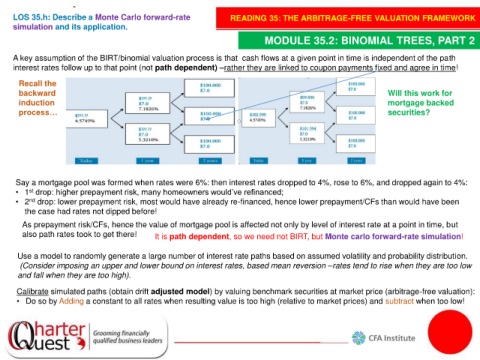

A key assumption of the BIRT/binomial valuation process is that cash flows at a given point in time is independent of the path

interest rates follow up to that point (not path dependent) –rather they are linked to coupon payments fixed and agree in time!

Recall the

backward Will this work for

induction mortgage backed

process… securities?

Say a mortgage pool was formed when rates were 6%: then interest rates dropped to 4%, rose to 6%, and dropped again to 4%:

st

• 1 drop: higher prepayment risk, many homeowners would’ve refinanced;

• 2 nd drop: lower prepayment risk, most would have already re-financed, hence lower prepayment/CFs than would have been

the case had rates not dipped before!

As prepayment risk/CFs, hence the value of mortgage pool is affected not only by level of interest rate at a point in time, but

also path rates took to get there! It is path dependent, so we need not BIRT, but Monte carlo forward-rate simulation!

Use a model to randomly generate a large number of interest rate paths based on assumed volatility and probability distribution.

(Consider imposing an upper and lower bound on interest rates, based mean reversion –rates tend to rise when they are too low

and fall when they are too high).

Calibrate simulated paths (obtain drift adjusted model) by valuing benchmark securities at market price (arbitrage-free valuation):

• Do so by Adding a constant to all rates when resulting value is too high (relative to market prices) and subtract when too low!