Page 10 - Improved +Example+Assessment+Report (LG Accrual) {FlipBook Test v1}_Neat (Online upload)

P. 10

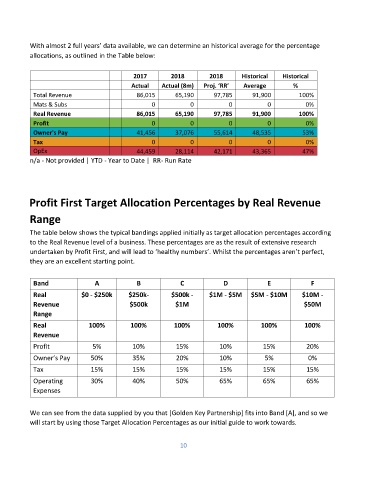

With almost 2 full years’ data available, we can determine an historical average for the percentage

allocations, as outlined in the Table below:

2017 2018 2018 Historical Historical

Actual Actual (8m) Proj. ‘RR’ Average %

Total Revenue 86,015 65,190 97,785 91,900 100%

Mats & Subs 0 0 0 0 0%

Real Revenue 86,015 65,190 97,785 91,900 100%

Profit 0 0 0 0 0%

Owner's Pay 41,456 37,076 55,614 48,535 53%

Tax 0 0 0 0 0%

OpEx 44,459 28,114 42,171 43,365 47%

n/a - Not provided | YTD - Year to Date | RR- Run Rate

Profit First Target Allocation Percentages by Real Revenue

Range

The table below shows the typical bandings applied initially as target allocation percentages according

to the Real Revenue level of a business. These percentages are as the result of extensive research

undertaken by Profit First, and will lead to ‘healthy numbers’. Whilst the percentages aren’t perfect,

they are an excellent starting point.

Band A B C D E F

Real $0 - $250k $250k- $500k - $1M - $5M $5M - $10M $10M -

Revenue $500k $1M $50M

Range

Real 100% 100% 100% 100% 100% 100%

Revenue

Profit 5% 10% 15% 10% 15% 20%

Owner’s Pay 50% 35% 20% 10% 5% 0%

Tax 15% 15% 15% 15% 15% 15%

Operating 30% 40% 50% 65% 65% 65%

Expenses

We can see from the data supplied by you that [Golden Key Partnership] fits into Band [A], and so we

will start by using those Target Allocation Percentages as our initial guide to work towards.

10