Page 33 - AR_NorthSuburbs_Mobile

P. 33

2019 Tax Rate Scenario

Property Tax Scenario: Fairness

In the last section we showed how changes in a taxing district’s property tax extension and

Equalized Assessed Value affected its property tax rate and the bills paid by property owners.

The values used to determine your property tax rate and bill are initially estimated by the CCAO

and adjusted with CCAO appeals. However, the CCAO is not the final arbiter in determining

individual and total assessed values. After values are finalized by the CCAO, they are subject to

modification by the Cook County Board of Review (BOR) before the tax rate is calculated.

Stage 1: 2018 → Stage 2: 2019 CCAO Final Values → Stage 3: 2019 BOR Final Values

2018 Commercial Assessment Quality and 2019 Reassessments

The CCAO’s commitment is to fairness and accuracy in assessed values for all property

classes, so that no property is taxed more or less than its fair share. Historically, Cook County’s

3

assessment system has failed to meet this standard. An external audit by the International

Association of Assessing Officers (IAAO) conducted a study on commercial properties

throughout Cook County. They collected the 2018 estimated Fair Market Values finalized by the

4

BOR for every commercial property, and compared these estimated values to sale prices in

2018. By industry standards, estimated values should be reasonably close to actual sale prices.

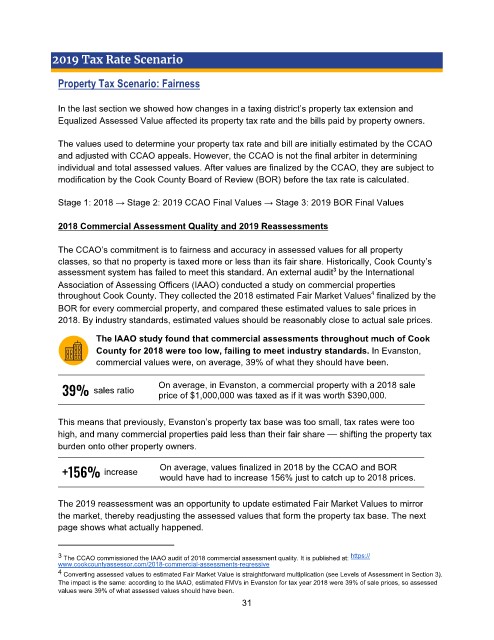

The IAAO study found that commercial assessments throughout much of Cook

County for 2018 were too low, failing to meet industry standards. In Evanston,

commercial values were, on average, 39% of what they should have been.

39% sales ratio On average, in Evanston, a commercial property with a 2018 sale

price of $1,000,000 was taxed as if it was worth $390,000.

This means that previously, Evanston’s property tax base was too small, tax rates were too

high, and many commercial properties paid less than their fair share — shifting the property tax

burden onto other property owners.

+156% increase On average, values finalized in 2018 by the CCAO and BOR

would have had to increase 156% just to catch up to 2018 prices.

The 2019 reassessment was an opportunity to update estimated Fair Market Values to mirror

the market, thereby readjusting the assessed values that form the property tax base. The next

page shows what actually happened.

3 The CCAO commissioned the IAAO audit of 2018 commercial assessment quality. It is published at: https://

www.cookcountyassessor.com/2018-commercial-assessments-regressive

4 Converting assessed values to estimated Fair Market Value is straightforward multiplication (see Levels of Assessment in Section 3).

The impact is the same: according to the IAAO, estimated FMVs in Evanston for tax year 2018 were 39% of sale prices, so assessed

values were 39% of what assessed values should have been.

31