Page 283 - JoFA_2022

P. 283

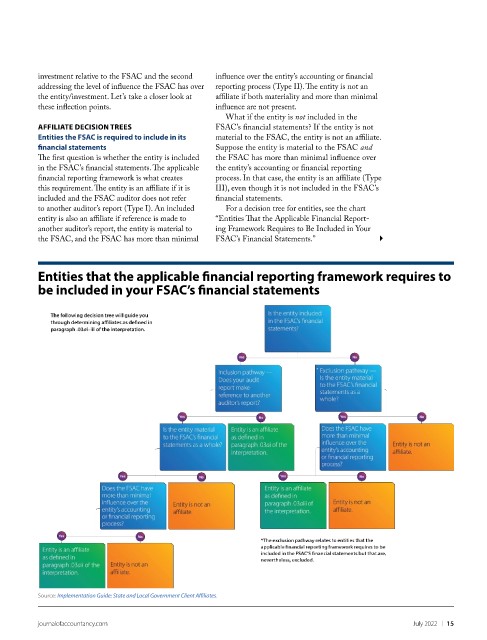

investment relative to the FSAC and the second influence over the entity’s accounting or financial

addressing the level of influence the FSAC has over reporting process (Type II). The entity is not an

the entity/investment. Let’s take a closer look at affiliate if both materiality and more than minimal

these inflection points. influence are not present.

What if the entity is not included in the

AFFILIATE DECISION TREES FSAC’s financial statements? If the entity is not

Entities the FSAC is required to include in its material to the FSAC, the entity is not an affiliate.

financial statements Suppose the entity is material to the FSAC and

The first question is whether the entity is included the FSAC has more than minimal influence over

in the FSAC’s financial statements. The applicable the entity’s accounting or financial reporting

financial reporting framework is what creates process. In that case, the entity is an affiliate (Type

this requirement. The entity is an affiliate if it is III), even though it is not included in the FSAC’s

included and the FSAC auditor does not refer financial statements.

to another auditor’s report (Type I). An included For a decision tree for entities, see the chart

entity is also an affiliate if reference is made to “Entities That the Applicable Financial Report-

another auditor’s report, the entity is material to ing Framework Requires to Be Included in Your

the FSAC, and the FSAC has more than minimal FSAC’s Financial Statements.”

Entities that the applicable financial reporting framework requires to

be included in your FSAC’s financial statements

Source: Implementation Guide: State and Local Government Client Affiliates.

journalofaccountancy.com July 2022 | 15