Page 284 - JoFA_2022

P. 284

AUDITING

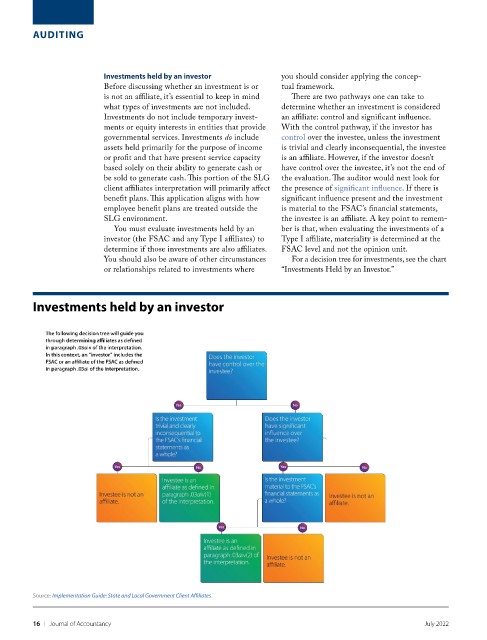

Investments held by an investor you should consider applying the concep-

Before discussing whether an investment is or tual framework.

is not an affiliate, it’s essential to keep in mind There are two pathways one can take to

what types of investments are not included. determine whether an investment is considered

Investments do not include temporary invest- an affiliate: control and significant influence.

ments or equity interests in entities that provide With the control pathway, if the investor has

governmental services. Investments do include control over the investee, unless the investment

assets held primarily for the purpose of income is trivial and clearly inconsequential, the investee

or profit and that have present service capacity is an affiliate. However, if the investor doesn’t

based solely on their ability to generate cash or have control over the investee, it’s not the end of

be sold to generate cash. This portion of the SLG the evaluation. The auditor would next look for

client affiliates interpretation will primarily affect the presence of significant influence. If there is

benefit plans. This application aligns with how significant influence present and the investment

employee benefit plans are treated outside the is material to the FSAC’s financial statements,

SLG environment. the investee is an affiliate. A key point to remem-

You must evaluate investments held by an ber is that, when evaluating the investments of a

investor (the FSAC and any Type I affiliates) to Type I affiliate, materiality is determined at the

determine if those investments are also affiliates. FSAC level and not the opinion unit.

You should also be aware of other circumstances For a decision tree for investments, see the chart

or relationships related to investments where “Investments Held by an Investor.”

Investments held by an investor

Source: Implementation Guide: State and Local Government Client Affiliates.

16 | Journal of Accountancy July 2022