Page 85 - JoFA_2022

P. 85

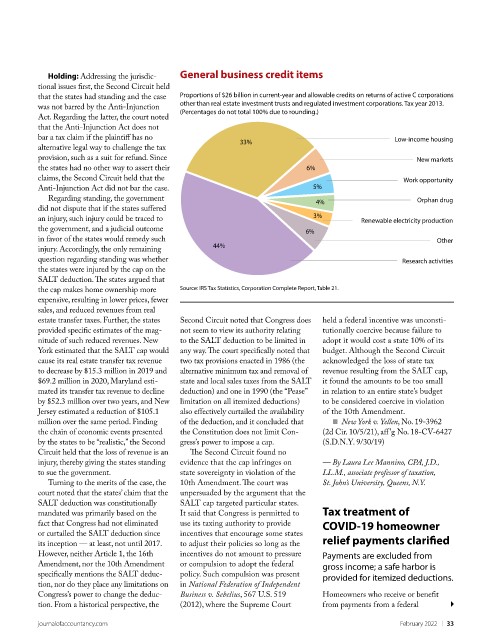

General business credit items

Holding: Addressing the jurisdic-

tional issues first, the Second Circuit held

Proportions of $26 billion in current-year and allowable credits on returns of active C corporations

that the states had standing and the case

other than real estate investment trusts and regulated investment corporations. Tax year 2013.

was not barred by the Anti-Injunction

(Percentages do not total 100% due to rounding.)

Act. Regarding the latter, the court noted

that the Anti-Injunction Act does not

bar a tax claim if the plaintiff has no Low-income housing

33%

alternative legal way to challenge the tax

provision, such as a suit for refund. Since New markets

the states had no other way to assert their 6%

claims, the Second Circuit held that the Work opportunity

Anti-Injunction Act did not bar the case. 5%

Regarding standing, the government Orphan drug

4%

did not dispute that if the states suffered

3%

an injury, such injury could be traced to Renewable electricity production

the government, and a judicial outcome 6%

in favor of the states would remedy such Other

44%

injury. Accordingly, the only remaining

question regarding standing was whether Research activities

the states were injured by the cap on the

SALT deduction. The states argued that

Source: IRS Tax Statistics, Corporation Complete Report, Table 21.

the cap makes home ownership more

expensive, resulting in lower prices, fewer

sales, and reduced revenues from real

estate transfer taxes. Further, the states Second Circuit noted that Congress does held a federal incentive was unconsti-

provided specific estimates of the mag- not seem to view its authority relating tutionally coercive because failure to

nitude of such reduced revenues. New to the SALT deduction to be limited in adopt it would cost a state 10% of its

York estimated that the SALT cap would any way. The court specifically noted that budget. Although the Second Circuit

cause its real estate transfer tax revenue two tax provisions enacted in 1986 (the acknowledged the loss of state tax

to decrease by $15.3 million in 2019 and alternative minimum tax and removal of revenue resulting from the SALT cap,

$69.2 million in 2020, Maryland esti- state and local sales taxes from the SALT it found the amounts to be too small

mated its transfer tax revenue to decline deduction) and one in 1990 (the “Pease” in relation to an entire state’s budget

by $52.3 million over two years, and New limitation on all itemized deductions) to be considered coercive in violation

Jersey estimated a reduction of $105.1 also effectively curtailed the availability of the 10th Amendment.

million over the same period. Finding of the deduction, and it concluded that ■ New York v. Yellen, No. 19-3962

the chain of economic events presented the Constitution does not limit Con- (2d Cir. 10/5/21), aff’g No. 18-CV-6427

by the states to be “realistic,” the Second gress’s power to impose a cap. (S.D.N.Y. 9/30/19)

Circuit held that the loss of revenue is an The Second Circuit found no

injury, thereby giving the states standing evidence that the cap infringes on — By Laura Lee Mannino, CPA, J.D.,

to sue the government. state sovereignty in violation of the LL.M., associate professor of taxation,

Turning to the merits of the case, the 10th Amendment. The court was St. John’s University, Queens, N.Y.

court noted that the states’ claim that the unpersuaded by the argument that the

SALT deduction was constitutionally SALT cap targeted particular states.

mandated was primarily based on the It said that Congress is permitted to Tax treatment of

COVID-19 homeowner

fact that Congress had not eliminated use its taxing authority to provide

or curtailed the SALT deduction since incentives that encourage some states relief payments clarified

its inception — at least, not until 2017. to adjust their policies so long as the

However, neither Article 1, the 16th incentives do not amount to pressure Payments are excluded from

Amendment, nor the 10th Amendment or compulsion to adopt the federal gross income; a safe harbor is

specifically mentions the SALT deduc- policy. Such compulsion was present provided for itemized deductions.

tion, nor do they place any limitations on in National Federation of Independent

Congress’s power to change the deduc- Business v. Sebelius, 567 U.S. 519 Homeowners who receive or benefit

tion. From a historical perspective, the (2012), where the Supreme Court from payments from a federal

journalofaccountancy.com February 2022 | 33