Page 291 - ACFE Fraud Reports 2009_2020

P. 291

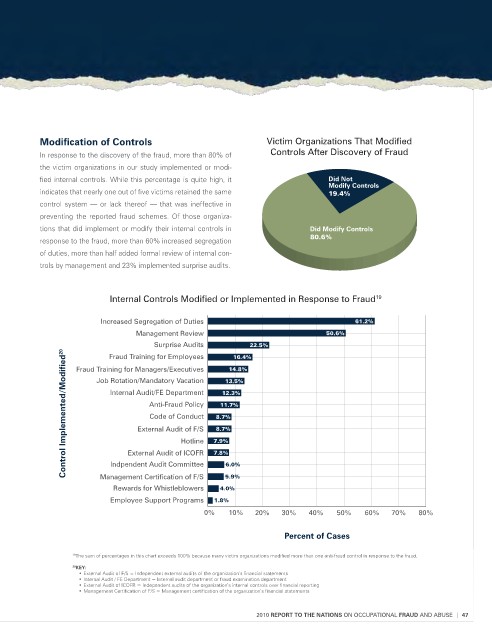

Modification of Controls Victim Organizations That Modified

In response to the discovery of the fraud, more than 80% of controls After discovery of Fraud

the victim organizations in our study implemented or modi-

fied internal controls. While this percentage is quite high, it Did Not

Modify Controls

indicates that nearly one out of five victims retained the same 19.4%

control system — or lack thereof — that was ineffective in

preventing the reported fraud schemes. Of those organiza-

tions that did implement or modify their internal controls in Did Modify Controls

response to the fraud, more than 60% increased segregation 80.6%

of duties, more than half added formal review of internal con-

trols by management and 23% implemented surprise audits.

Internal controls Modified or Implemented in Response to Fraud 19

Increased Segregation of Duties 61.2%

Management Review 50.6%

Surprise Audits 14.8% 22.5%

Control Implemented/Modified 20 Job Rotation/Mandatory Vacation 7.9% 13.5%

Fraud Training for Employees

16.4%

Fraud Training for Managers/Executives

Internal Audit/FE Department

12.3%

Anti-Fraud Policy

11.7%

Code of Conduct

8.7%

External Audit of F/S

8.7%

Hotline

External Audit of ICOFR

Indpendent Audit Committee

6.0%

Management Certification of F/S

Rewards for Whistleblowers 7.8% 5.9%

4.0%

Employee Support Programs 1.8%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Percent of Cases

19 The sum of percentages in this chart exceeds 100% because many victim organizations modified more than one anti-fraud control in response to the fraud.

20 KeY:

• External Audit of F/S = Independent external audits of the organization’s financial statements

• Internal Audit / FE Department = Internal audit department or fraud examination department

• External Audit of ICOFR = Independent audits of the organization’s internal controls over financial reporting

• Management Certification of F/S = Management certification of the organization’s financial statements

2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE | 47