Page 288 - ACFE Fraud Reports 2009_2020

P. 288

Victim organizations

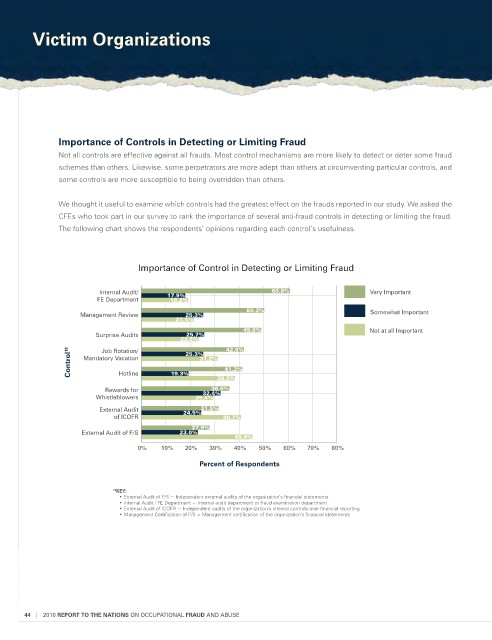

importance of Controls in Detecting or Limiting Fraud

Not all controls are effective against all frauds. Most control mechanisms are more likely to detect or deter some fraud

schemes than others. Likewise, some perpetrators are more adept than others at circumventing particular controls, and

some controls are more susceptible to being overridden than others.

We thought it useful to examine which controls had the greatest effect on the frauds reported in our study. We asked the

CFEs who took part in our survey to rank the importance of several anti-fraud controls in detecting or limiting the fraud.

The following chart shows the respondents’ opinions regarding each control’s usefulness.

Importance of control in detecting or limiting Fraud

Internal Audit/ 17.9% 60.8% Very Important

FE Department 19.2%

50.3% Somewhat Important

Management Review 25.3%

21.4%

49.0% Not at all Important

Surprise Audits 25.7%

23.5% 42.0%

Job Rotation/

Control 18 Mandatory Vacation 19.3% 25.3% 31.2% 41.3%

Hotline

36.0%

Rewards for 32.4% 38.3%

Whistleblowers 29.4%

External Audit 24.5% 31.5%

of ICOFR 40.7%

27.9%

External Audit of F/S 23.0%

45.4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Percent of Respondents

18 KeY:

• External Audit of F/S = Independent external audits of the organization’s financial statements

• Internal Audit / FE Department = Internal audit department or fraud examination department

• External Audit of ICOFR = Independent audits of the organization’s internal controls over financial reporting

• Management Certification of F/S = Management certification of the organization’s financial statements

44 | 2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE