Page 346 - ACFE Fraud Reports 2009_2020

P. 346

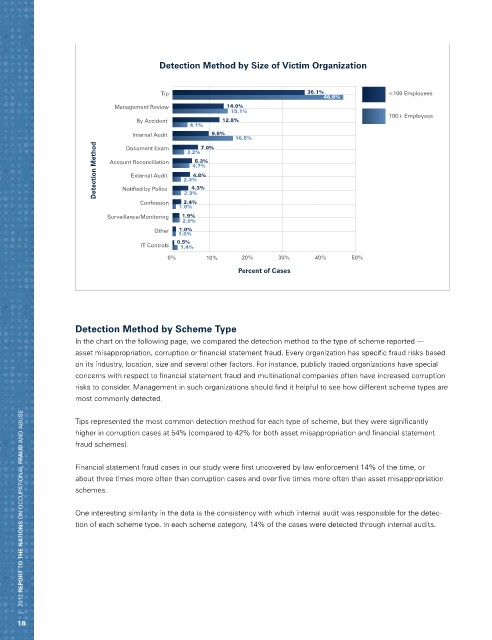

Detection Method by Size of Victim Organization

Tip 36.1% <100 Employees

46.6%

Management Review 14.0%

15.1%

100+ Employees

By Accident 12.8%

4.1%

Internal Audit 9.9%

16.5%

Detection Method Account Reconciliation 2.3% 4.8%

Document Exam

7.0%

3.2%

5.3%

4.7%

External Audit

4.3%

Notified by Police

2.3%

Confession 2.4%

1.0%

Surveillance/Monitoring 1.9%

2.0%

Other 1.0%

1.0%

0.5%

IT Controls 1.4%

0% 10% 20% 30% 40% 50%

Percent of Cases

Detection Method by Scheme Type

In the chart on the following page, we compared the detection method to the type of scheme reported —

asset misappropriation, corruption or financial statement fraud. Every organization has specific fraud risks based

on its industry, location, size and several other factors. For instance, publicly traded organizations have special

concerns with respect to financial statement fraud and multinational companies often have increased corruption

risks to consider. Management in such organizations should find it helpful to see how different scheme types are

most commonly detected.

| 2012 REPORT TO THE NATIONS on occupational FRAUD and abuse

Tips represented the most common detection method for each type of scheme, but they were significantly

higher in corruption cases at 54% (compared to 42% for both asset misappropriation and financial statement

fraud schemes).

Financial statement fraud cases in our study were first uncovered by law enforcement 14% of the time, or

about three times more often than corruption cases and over five times more often than asset misappropriation

schemes.

One interesting similarity in the data is the consistency with which internal audit was responsible for the detec-

tion of each scheme type. In each scheme category, 14% of the cases were detected through internal audits.

18