Page 344 - ACFE Fraud Reports 2009_2020

P. 344

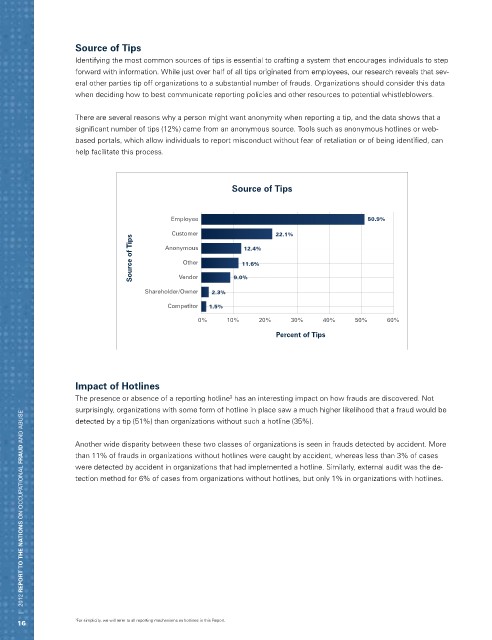

Source of Tips

Identifying the most common sources of tips is essential to crafting a system that encourages individuals to step

forward with information. While just over half of all tips originated from employees, our research reveals that sev-

eral other parties tip off organizations to a substantial number of frauds. Organizations should consider this data

when deciding how to best communicate reporting policies and other resources to potential whistleblowers.

There are several reasons why a person might want anonymity when reporting a tip, and the data shows that a

significant number of tips (12%) came from an anonymous source. Tools such as anonymous hotlines or web-

based portals, which allow individuals to report misconduct without fear of retaliation or of being identified, can

help facilitate this process.

Source of Tips

Employee 50.9%

Customer 22.1%

Source of Tips Anonymous 11.6%

12.4%

Other

Vendor

Shareholder/Owner 2.3% 9.0%

Competitor 1.5%

0% 10% 20% 30% 40% 50% 60%

Percent of Tips

Impact of Hotlines

The presence or absence of a reporting hotline has an interesting impact on how frauds are discovered. Not

3

surprisingly, organizations with some form of hotline in place saw a much higher likelihood that a fraud would be

| 2012 REPORT TO THE NATIONS on occupational FRAUD and abuse

detected by a tip (51%) than organizations without such a hotline (35%).

Another wide disparity between these two classes of organizations is seen in frauds detected by accident. More

than 11% of frauds in organizations without hotlines were caught by accident, whereas less than 3% of cases

were detected by accident in organizations that had implemented a hotline. Similarly, external audit was the de-

tection method for 6% of cases from organizations without hotlines, but only 1% in organizations with hotlines.

16 3 For simplicity, we will refer to all reporting mechanisms as hotlines in this Report.