Page 345 - ACFE Fraud Reports 2009_2020

P. 345

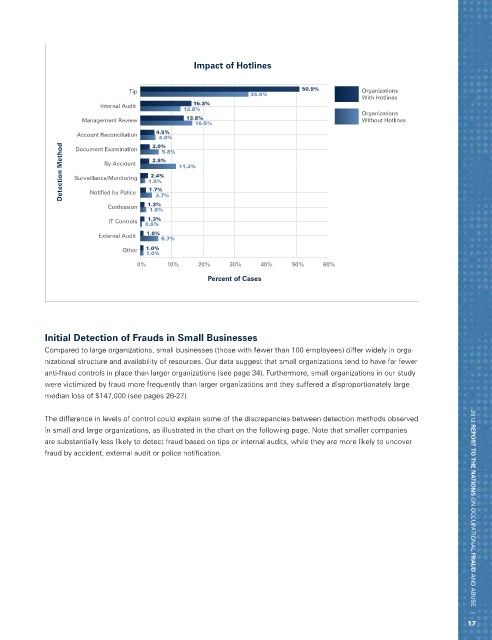

Impact of Hotlines

Tip 50.9% Organizations

34.6%

With Hotlines

Internal Audit 16.3%

12.8% Organizations

Management Review 13.8% Without Hotlines

16.5%

4.5%

Account Reconciliation 3.0%

4.8%

Detection Method Surveillance/Monitoring 1.5% 11.3%

Document Examination

5.8%

2.8%

By Accident

2.4%

1.7%

Notified by Police

3.7%

Confession 1.3%

1.8%

1.3%

IT Controls 0.5%

External Audit 1.0% 5.7%

Other 1.0%

1.0%

0% 10% 20% 30% 40% 50% 60%

Percent of Cases

Initial Detection of Frauds in Small Businesses

Compared to large organizations, small businesses (those with fewer than 100 employees) differ widely in orga-

nizational structure and availability of resources. Our data suggest that small organizations tend to have far fewer

anti-fraud controls in place than larger organizations (see page 34). Furthermore, small organizations in our study

were victimized by fraud more frequently than larger organizations and they suffered a disproportionately large

median loss of $147,000 (see pages 26-27).

The difference in levels of control could explain some of the discrepancies between detection methods observed

in small and large organizations, as illustrated in the chart on the following page. Note that smaller companies

are substantially less likely to detect fraud based on tips or internal audits, while they are more likely to uncover

fraud by accident, external audit or police notification. 2012 REPORT TO THE NATIONS on occupational FRAUD and abuse |

17