Page 451 - ACFE Fraud Reports 2009_2020

P. 451

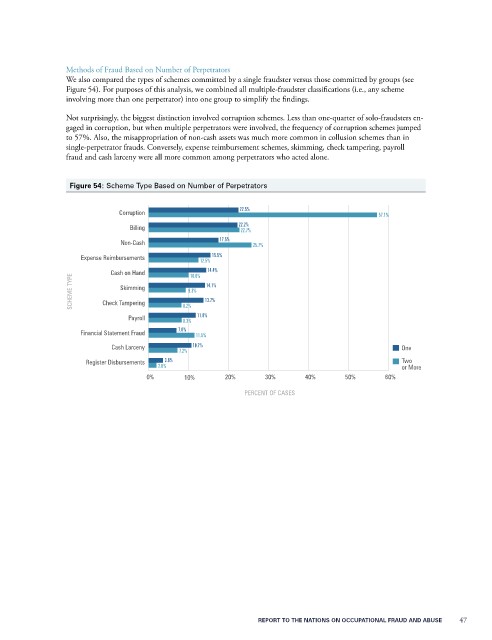

Methods of Fraud Based on Number of Perpetrators

We also compared the types of schemes committed by a single fraudster versus those committed by groups (see

Figure 54). For purposes of this analysis, we combined all multiple-fraudster classifications (i.e., any scheme

involving more than one perpetrator) into one group to simplify the findings.

Not surprisingly, the biggest distinction involved corruption schemes. Less than one-quarter of solo-fraudsters en-

gaged in corruption, but when multiple perpetrators were involved, the frequency of corruption schemes jumped

to 57%. Also, the misappropriation of non-cash assets was much more common in collusion schemes than in

single-perpetrator frauds. Conversely, expense reimbursement schemes, skimming, check tampering, payroll

fraud and cash larceny were all more common among perpetrators who acted alone.

Figure 54: Scheme Type Based on Number of Perpetrators

Corruption 22.5% 57.1%

Billing 22.2%

22.7%

Non-Cash 17.5% 25.7%

Expense Reimbursements 12.5% 15.5%

Cash on Hand 10.0% 14.4%

SCHEME TYPE Check Tampering 9.3% 13.7%

14.1%

Skimming

Payroll 8.2% 11.8%

8.3%

Financial Statement Fraud 7.0% 11.5%

Cash Larceny 10.7% One

7.2%

Register Disbursements 3.6% Two

2.0% or More

0% 10% 20% 30% 40% 50% 60%

PERCENT OF CASES

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 47