Page 455 - ACFE Fraud Reports 2009_2020

P. 455

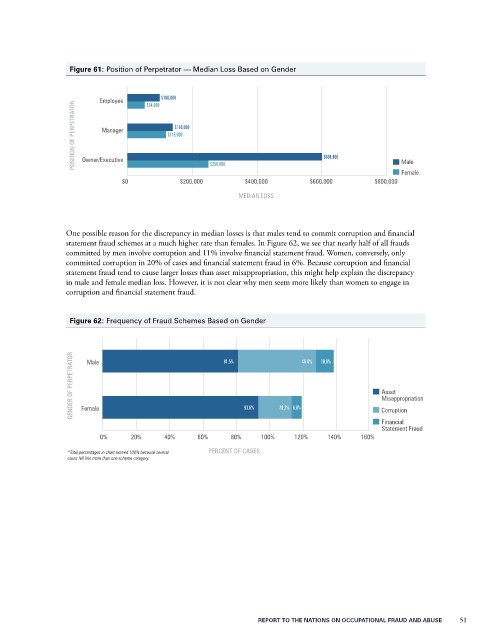

Figure 61: Position of Perpetrator — Median Loss Based on Gender

Employee $54,000 $100,000

POSITION OF PERPETRATOR Manager $119,000

$140,000

$600,000

Owner/Executive

Male

$250,000

Female

$0 $200,000 $400,000 $600,000 $800,000

MEDIAN LOSS

One possible reason for the discrepancy in median losses is that males tend to commit corruption and financial

statement fraud schemes at a much higher rate than females. In Figure 62, we see that nearly half of all frauds

committed by men involve corruption and 11% involve financial statement fraud. Women, conversely, only

committed corruption in 20% of cases and financial statement fraud in 6%. Because corruption and financial

statement fraud tend to cause larger losses than asset misappropriation, this might help explain the discrepancy

in male and female median loss. However, it is not clear why men seem more likely than women to engage in

corruption and financial statement fraud.

Figure 62: Frequency of Fraud Schemes Based on Gender

GENDER OF PERPETRATOR Male 81.5% 46.8% 10.6% Asset

Misappropriation

20.2% 6.0%

Female

93.6%

Corruption

Financial

Statement Fraud

0% 20% 40% 60% 80% 100% 120% 140% 160%

*Total percentages in chart exceed 100% because several PERCENT OF CASES

cases fell into more than one scheme category.

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 51