Page 675 - ACFE Fraud Reports 2009_2020

P. 675

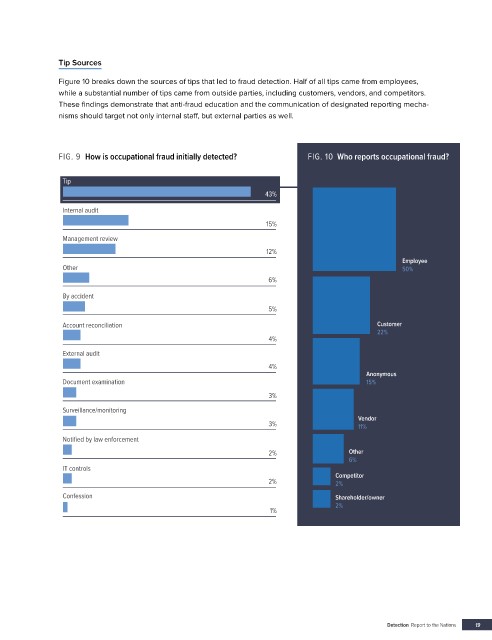

Tip Sources

Figure 10 breaks down the sources of tips that led to fraud detection. Half of all tips came from employees,

while a substantial number of tips came from outside parties, including customers, vendors, and competitors.

These findings demonstrate that anti-fraud education and the communication of designated reporting mecha-

nisms should target not only internal staff, but external parties as well.

FIG. 9 How is occupational fraud initially detected? FIG. 10 Who reports occupational fraud?

Tip

43%

Internal audit

15%

Management review

12%

Employee

Other 50%

6%

By accident

5%

Account reconciliation Customer

22%

4%

External audit

4%

Anonymous

Document examination 15%

3%

Surveillance/monitoring

Vendor

3% 11%

Notified by law enforcement

2% Other

6%

IT controls

Competitor

2% 2%

Confession Shareholder/owner

2%

1%

Detection Report to the Nations 19