Page 679 - ACFE Fraud Reports 2009_2020

P. 679

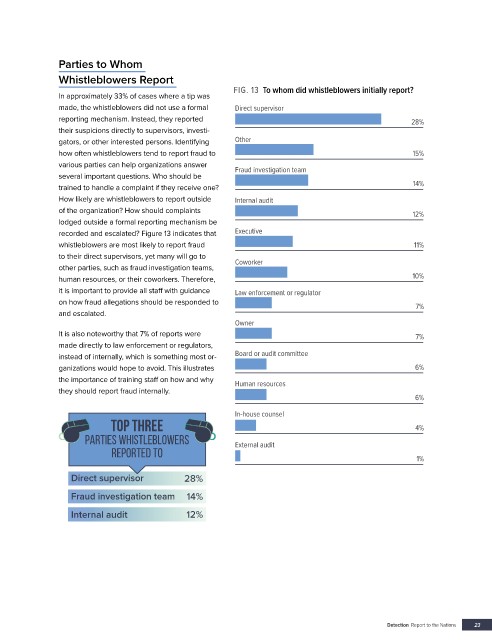

Parties to Whom

Whistleblowers Report

FIG. 13 To whom did whistleblowers initially report?

In approximately 33% of cases where a tip was

made, the whistleblowers did not use a formal Direct supervisor

reporting mechanism. Instead, they reported 28%

their suspicions directly to supervisors, investi-

gators, or other interested persons. Identifying Other

how often whistleblowers tend to report fraud to 15%

various parties can help organizations answer Fraud investigation team

several important questions. Who should be

trained to handle a complaint if they receive one? 14%

How likely are whistleblowers to report outside Internal audit

of the organization? How should complaints 12%

lodged outside a formal reporting mechanism be

recorded and escalated? Figure 13 indicates that Executive

whistleblowers are most likely to report fraud 11%

to their direct supervisors, yet many will go to Coworker

other parties, such as fraud investigation teams,

human resources, or their coworkers. Therefore, 10%

it is important to provide all staff with guidance Law enforcement or regulator

on how fraud allegations should be responded to 7%

and escalated.

Owner

It is also noteworthy that 7% of reports were 7%

made directly to law enforcement or regulators,

instead of internally, which is something most or- Board or audit committee

ganizations would hope to avoid. This illustrates 6%

the importance of training staff on how and why Human resources

they should report fraud internally.

6%

In-house counsel

TOP THREE 4%

Parties whistleblowers External audit

reported to 1%

Direct supervisor 28%

Fraud investigation team 14%

Internal audit 12%

Detection Report to the Nations 23