Page 696 - ACFE Fraud Reports 2009_2020

P. 696

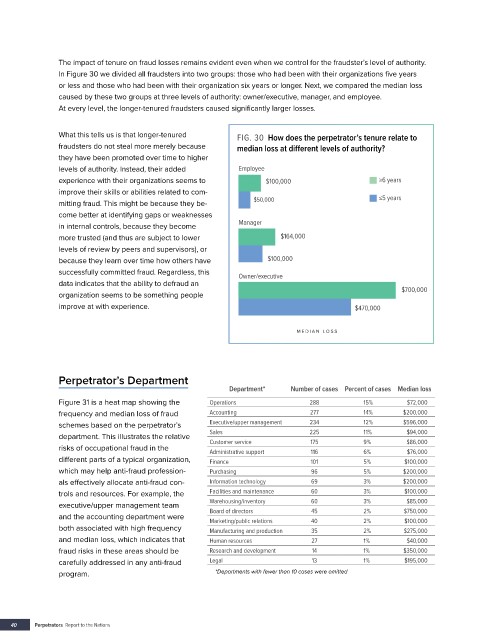

The impact of tenure on fraud losses remains evident even when we control for the fraudster’s level of authority.

In Figure 30 we divided all fraudsters into two groups: those who had been with their organizations five years

or less and those who had been with their organization six years or longer. Next, we compared the median loss

caused by these two groups at three levels of authority: owner/executive, manager, and employee.

At every level, the longer-tenured fraudsters caused significantly larger losses.

What this tells us is that longer-tenured FIG. 30 How does the perpetrator’s tenure relate to

fraudsters do not steal more merely because median loss at different levels of authority?

they have been promoted over time to higher

levels of authority. Instead, their added Employee

experience with their organizations seems to $100,000 ≥6 years

improve their skills or abilities related to com- ≤5 years

mitting fraud. This might be because they be- $50,000

come better at identifying gaps or weaknesses

in internal controls, because they become Manager

more trusted (and thus are subject to lower $164,000

levels of review by peers and supervisors), or

because they learn over time how others have $100,000

successfully committed fraud. Regardless, this Owner/executive

data indicates that the ability to defraud an $700,000

organization seems to be something people

improve at with experience. $470,000

MEDIAN L OSS

Perpetrator’s Department

Department* Number of cases Percent of cases Median loss

Figure 31 is a heat map showing the Operations 288 15% $72,000

frequency and median loss of fraud Accounting 277 14% $200,000

schemes based on the perpetrator’s Executive/upper management 234 12% $596,000

$94,000

department. This illustrates the relative Sales 225 11% $86,000

9%

175

Customer service

risks of occupational fraud in the Administrative support 116 6% $76,000

different parts of a typical organization, Finance 101 5% $100,000

which may help anti-fraud profession- Purchasing 96 5% $200,000

als effectively allocate anti-fraud con- Information technology 69 3% $200,000

trols and resources. For example, the Facilities and maintenance 60 3% $100,000

$85,000

executive/upper management team Warehousing/inventory 60 3% $750,000

Board of directors

45

2%

and the accounting department were Marketing/public relations 40 2% $100,000

both associated with high frequency Manufacturing and production 35 2% $275,000

and median loss, which indicates that Human resources 27 1% $40,000

fraud risks in these areas should be Research and development 14 1% $350,000

carefully addressed in any anti-fraud Legal 13 1% $195,000

program. *Departments with fewer than 10 cases were omitted

40 Perpetrators Report to the Nations