Page 94 - ACFE Fraud Reports 2009_2020

P. 94

Table of Contents

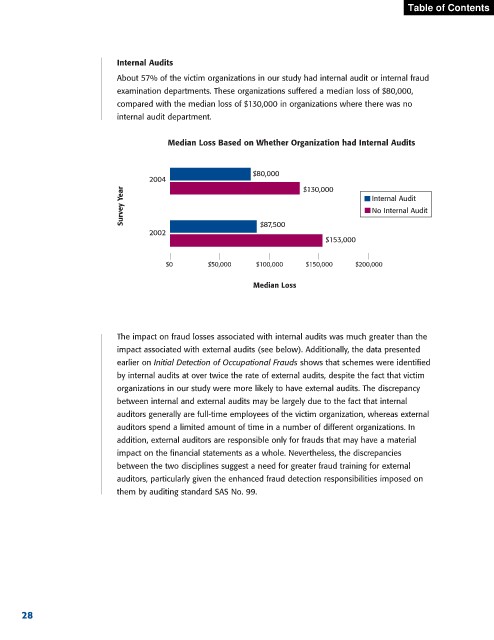

Internal Audits

About 57% of the victim organizations in our study had internal audit or internal fraud

examination departments. These organizations suffered a median loss of $80,000,

compared with the median loss of $130,000 in organizations where there was no

internal audit department.

Median Loss Based on Whether Organization had Internal Audits

$80,000

2004 $130,000

Survey Year Internal Audit

No Internal Audit

2002 $87,500

$153,000

$0 $50,000 $100,000 $150,000 $200,000

Median Loss

The impact on fraud losses associated with internal audits was much greater than the

impact associated with external audits (see below). Additionally, the data presented

earlier on Initial Detection of Occupational Frauds shows that schemes were identified

by internal audits at over twice the rate of external audits, despite the fact that victim

organizations in our study were more likely to have external audits. The discrepancy

between internal and external audits may be largely due to the fact that internal

auditors generally are full-time employees of the victim organization, whereas external

auditors spend a limited amount of time in a number of different organizations. In

addition, external auditors are responsible only for frauds that may have a material

impact on the financial statements as a whole. Nevertheless, the discrepancies

between the two disciplines suggest a need for greater fraud training for external

auditors, particularly given the enhanced fraud detection responsibilities imposed on

them by auditing standard SAS No. 99.

External Audits

The most common anti-fraud measure among the victims in our study was the external

audit. Seventy-five percent of victims employed independent auditors. However, the

effectiveness of external audits in reducing fraud losses was not observable in our

study. In fact, the median loss was actually higher in organizations that had external

audits, as opposed to those that did not. Of course, there are several factors that

contribute to the presence and size of fraud. But it was disappointing to find no trend

28