Page 91 - ACFE Fraud Reports 2009_2020

P. 91

Table of Contents

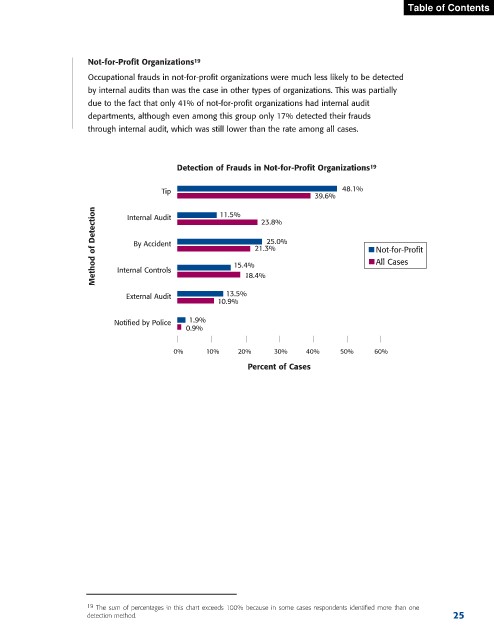

Not-for-Profit Organizations 19

Occupational frauds in not-for-profit organizations were much less likely to be detected

by internal audits than was the case in other types of organizations. This was partially

due to the fact that only 41% of not-for-profit organizations had internal audit

departments, although even among this group only 17% detected their frauds

through internal audit, which was still lower than the rate among all cases.

Detection of Frauds in Not-for-Profit Organizations 19

Tip 48.1%

39.6%

Method of Detection Internal Controls 15.4% 21.3% Not-for-Profit

11.5%

Internal Audit

23.8%

25.0%

By Accident

All Cases

External Audit 13.5% 18.4%

10.9%

Notified by Police 1.9%

0.9%

0% 10% 20% 30% 40% 50% 60%

Percent of Cases

19 The sum of percentages in this chart exceeds 100% because in some cases respondents identified more than one

detection method. 25