Page 95 - ACFE Fraud Reports 2009_2020

P. 95

Table of Contents

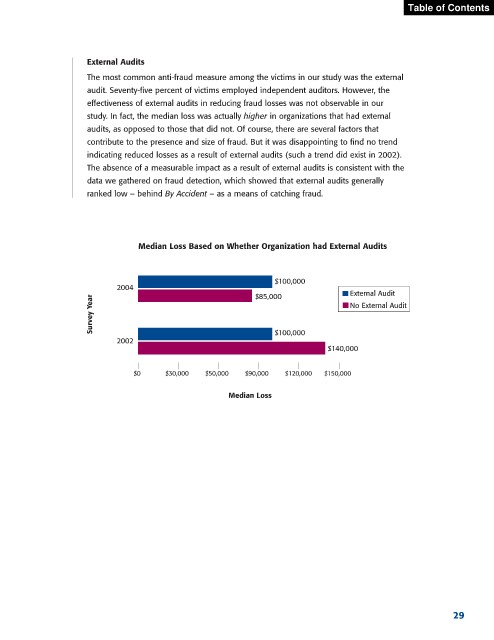

External Audits

The most common anti-fraud measure among the victims in our study was the external

audit. Seventy-five percent of victims employed independent auditors. However, the

effectiveness of external audits in reducing fraud losses was not observable in our

study. In fact, the median loss was actually higher in organizations that had external

audits, as opposed to those that did not. Of course, there are several factors that

contribute to the presence and size of fraud. But it was disappointing to find no trend

indicating reduced losses as a result of external audits (such a trend did exist in 2002).

The absence of a measurable impact as a result of external audits is consistent with the

data we gathered on fraud detection, which showed that external audits generally

ranked low – behind By Accident – as a means of catching fraud.

Median Loss Based on Whether Organization had External Audits

$100,000

2004 $85,000 External Audit

Survey Year No External Audit

2002 $100,000

$140,000

$0 $30,000 $50,000 $90,000 $120,000 $150,000

Median Loss

29