Page 92 - ACFE Fraud Reports 2009_2020

P. 92

Table of Contents

6 Limiting Fraud Losses

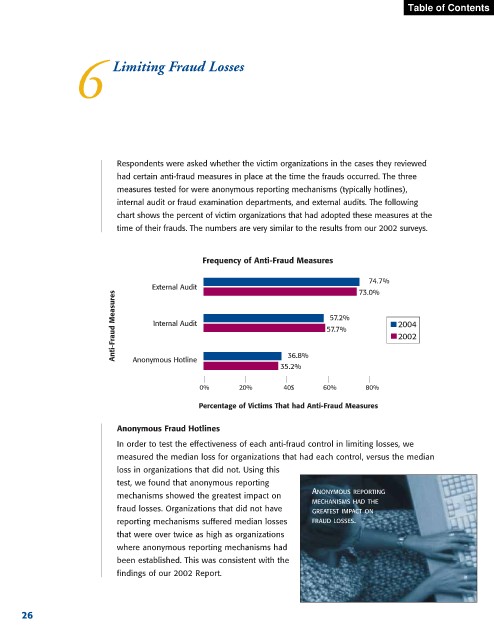

Respondents were asked whether the victim organizations in the cases they reviewed

had certain anti-fraud measures in place at the time the frauds occurred. The three

measures tested for were anonymous reporting mechanisms (typically hotlines),

internal audit or fraud examination departments, and external audits. The following

chart shows the percent of victim organizations that had adopted these measures at the

time of their frauds. The numbers are very similar to the results from our 2002 surveys.

Frequency of Anti-Fraud Measures

74.7%

External Audit 73.0%

Anti-Fraud Measures Internal Audit 57.7% 2004

57.2%

2002

36.8%

Anonymous Hotline

35.2%

0% 20% 40$ 60% 80%

Percentage of Victims That had Anti-Fraud Measures

Anonymous Fraud Hotlines

In order to test the effectiveness of each anti-fraud control in limiting losses, we

measured the median loss for organizations that had each control, versus the median

loss in organizations that did not. Using this

test, we found that anonymous reporting

ANONYMOUS REPORTING

mechanisms showed the greatest impact on

MECHANISMS HAD THE

fraud losses. Organizations that did not have GREATEST IMPACT ON

reporting mechanisms suffered median losses FRAUD LOSSES.

that were over twice as high as organizations

where anonymous reporting mechanisms had

been established. This was consistent with the

findings of our 2002 Report.

26